Modern suburban house with green lawn and a padlock attached to a percentage sign symbolizing fixed interest rate security

Fixed Rate Home Equity Loan Guide

Your home's worth more than when you bought it. Maybe a lot more. So how do you tap that growing equity without gambling on payment swings every time the Fed meets?

That's where fixed rate home equity loans come in—you borrow once, get the cash upfront, and your monthly bill never budges. No surprises when interest rates jump. No scrambling to adjust your budget when economic headlines turn scary.

But here's the catch: you'll probably pay more initially than with adjustable options. And if rates drop next year? You're stuck unless you want to refinance and eat another round of closing costs.

This guide walks through everything—how lenders price these loans, when the stability actually pays off, and what hoops you'll jump through to get approved.

What Is a Fixed Rate Home Equity Loan?

Picture a traditional car loan or personal loan, except your house backs it. The bank hands you a check for the full amount—let's say $40,000—and you pay it back in equal chunks every month for the next 10, 15, or 20 years. Your rate? Locked in on day one and never changes.

Here's a concrete example. You close on $50,000 at 7.5% for 15 years. Month one, you owe $463. Month 87? Still $463. Month 180? Same $463. Doesn't matter if inflation hits 8%, recession strikes, or the Fed drops rates to zero—your payment stays glued to that number. Each payment chips away at both interest and principal, slowly rebuilding the equity you borrowed against.

Author: Hannah Whitlock;

Source: isomfence.com

Now contrast that with a home equity line of credit. HELOCs work like credit cards tied to your property. You get a borrowing ceiling—say $75,000—that you can draw from and repay repeatedly over 10 years. Sounds flexible, right? It is. But there's a tradeoff: your rate adjusts monthly based on the prime rate. Pull $50,000 when prime's at 5%, and you might pay $208 in interest that month. Prime climbs to 7%? Now you're paying $292. That $84 jump happens automatically, no warning letter required.

When you close this type of loan, your lender files what's called a second lien against your title. Translation: if you stop paying and the bank forecloses, your original mortgage company gets paid first from whatever the house sells for. Because they're second in line, lenders cap how much you can borrow—usually 80–90% of your home's value when you add your existing mortgage and the new loan together.

How Fixed Home Equity Rates Work

Lenders don't pull your rate from thin air. They start with what 10-year Treasury bonds are yielding, then pile on adjustments based on three big factors: your credit score, how much equity you're leaving in the house, and what's happening in the broader economy.

Your credit score matters—a lot. Break 740 and you'll see lenders' best numbers. Sitting at 680? Expect them to tack on another 0.5% to 0.75%. Drop below 640 and you're either getting rejected outright or staring at rates in the double digits. One of my neighbors got quoted 6.9% with a 760 score. His brother-in-law with a 665 score? 8.2% from the same bank.

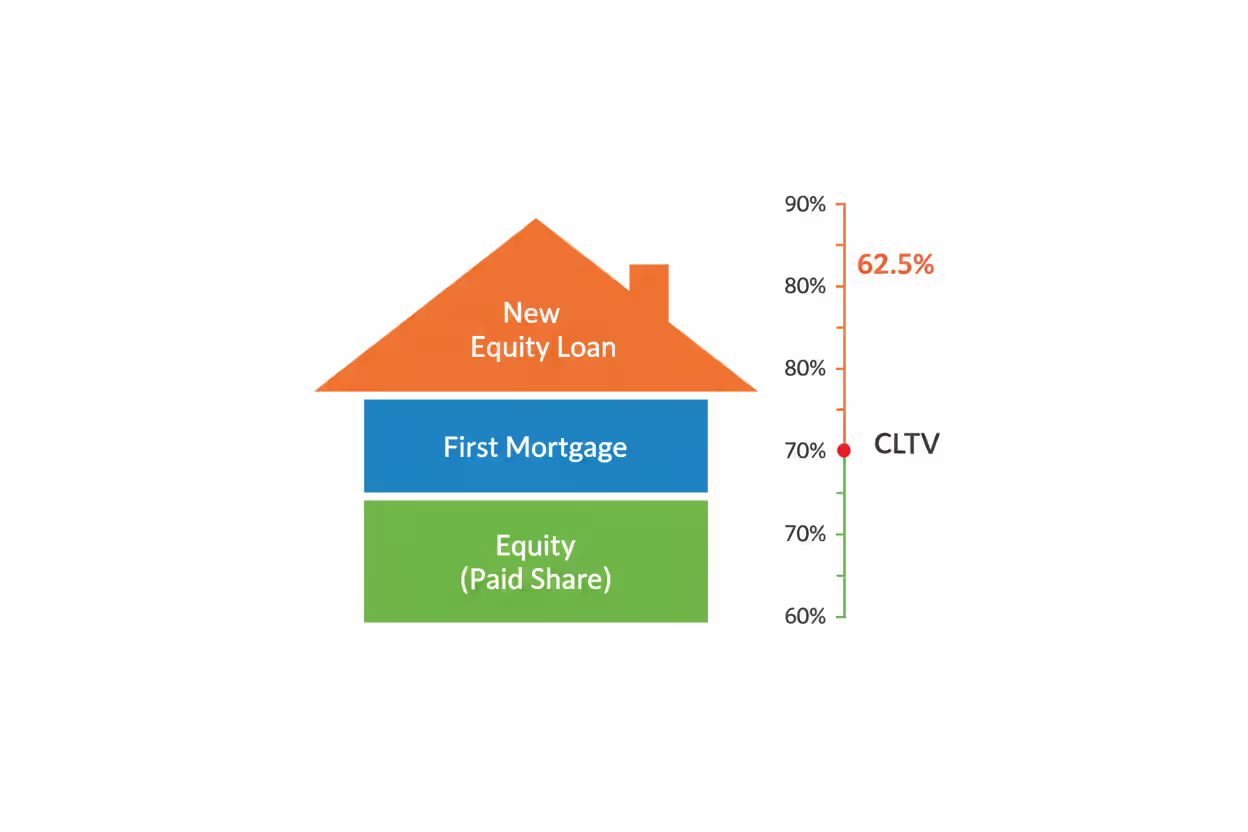

Loan-to-value calculations determine risk. Say your home appraises at $400,000. You owe $200,000 on your first mortgage and want to borrow $50,000. That puts your combined loan-to-value ratio at 62.5%—pretty safe territory. Lenders love that cushion. But stretch to $140,000 borrowed against that same house (85% CLTV) and suddenly you look riskier. That perception shift can cost you half a percentage point or more.

Author: Hannah Whitlock;

Source: isomfence.com

Market forces set the baseline. Treasury yields drive everything. As I'm writing this in early 2026, 10-year notes hover around 4.2%. Competitive fixed equity loans run between 6.75% and 9.5%, depending on your personal situation. When those Treasury rates jumped two points in 2022-2023, home equity pricing followed right along.

Once you sign on the dotted line, that rate becomes permanent—your entire repayment term. Lock in 7.25% this March and you'll still be paying 7.25% in March 2036, regardless of whether market rates skyrocket to 12% or crater to 4%. You're protected from increases but can't capture decreases without refinancing and paying new closing costs.

Fixed-rate home equity loans offer payment certainty that's especially valuable when the Federal Reserve is raising rates.Borrowers who locked 6.5% rates in late 2025 are already ahead of those who waited and now face 7.8% quotes

— Jennifer Kowalski

Fixed vs Variable Home Equity Loans

Which one makes sense? Depends on your tolerance for unpredictability, where you think rates are headed, and whether you need all the money right now or over time.

| Feature | Fixed Rate Loan | Variable Rate HELOC |

| How the rate behaves | Never changes after closing | Adjusts monthly, tied to prime rate |

| Monthly payment | Identical every billing cycle | Fluctuates—sometimes dramatically |

| When rates adjust | Never | Usually every 30 days |

| Makes most sense for | One-time expenses; when rates are climbing | Phased projects; falling rate environments |

| Your exposure | Budget-friendly but possibly pricier upfront | Uncertainty risk, often cheaper initially |

The certainty advantage: Fixed products eliminate guesswork. You know exactly what you'll owe in August 2027 and August 2035. HELOCs? They might start attractively—prime plus 0.5% could mean 5.75% today—but watch that number climb to 7.75% over two years as prime rises. That's an extra $50 per month in interest on just $30,000 outstanding.

How payments are structured: Fixed loans amortize fully, meaning every payment includes principal and interest from day one. Many HELOCs let you pay interest-only during the first 10 years, then suddenly require full principal-and-interest payments for the remaining term. That shift creates a payment shock totally separate from rate changes.

Risk profiles: Expecting rates to hold steady or climb? Fixed borrowing caps your total cost. Think the Fed will pivot and slash rates soon? An adjustable line lets you benefit automatically without refinancing paperwork.

Real situations:

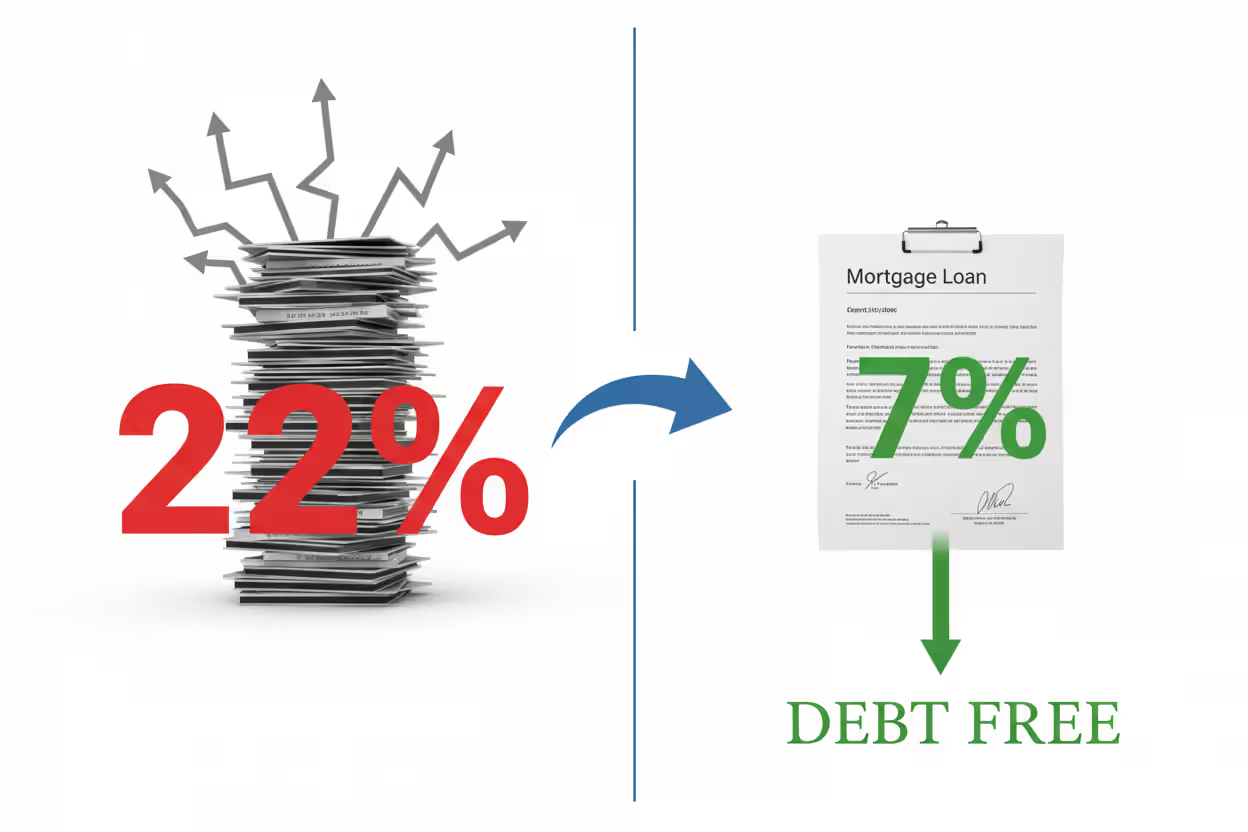

- Wiping out credit card debt: You're carrying $40,000 across cards at 22% average. Consolidate into a 7.5% fixed equity loan and you'll save roughly $580 monthly in interest charges alone. Stable payments help you stay on track instead of getting derailed by rate swings. - Remodeling over 18 months: A HELOC suits this better. Draw $15,000 for new cabinets in June, pull another $10,000 for appliances in October—you only pay interest on what you've actually used. If prime drops halfway through, your cost falls immediately.

Pros and Cons of Fixed Rate Equity Borrowing

What works in your favor:

- You can budget years ahead. Set up automatic payments and forget about it. No need to recalculate every month or brace for bad news when economic reports drop.

- Rate increases can't touch you. While your neighbor with a HELOC watches their payment climb $75, then $120, then $200 as the Fed keeps tightening, yours stays frozen.

- You rebuild equity from payment one. Those interest-only HELOCs? They postpone equity restoration for a decade. You're attacking principal immediately.

- Comparing lenders is straightforward. A 7.25% fixed quote means the same thing everywhere. Variable products require parsing margin structures, lifetime caps, and adjustment frequencies.

The downsides:

- You'll pay more upfront. Fixed structures typically run 0.5% to 1.5% higher than introductory HELOC rates. If rates fall next year, you're locked in unless you refinance.

- Less flexibility in borrowing. You get the full lump sum at closing whether you need it all immediately or not. Borrowed $60,000 but only spent $45,000 in year one? You're paying interest on that extra $15,000 sitting in your account.

- Refinancing costs real money. Chasing a better rate later means paying 2–5% of the loan amount in new closing costs—appraisals, title work, origination fees, the whole nine yards.

- Prepayment penalties lurk. Some lenders charge 2–3% of your remaining balance if you pay off within the first three to five years. Always check before signing.

You're essentially buying rate insurance. If stable budgets matter most and you expect rates to rise or stay flat, that premium's worth paying. If you're comfortable with volatility and anticipate rate drops, a flexible line might cost less despite the uncertainty.

When to Choose a Fixed Rate Home Equity Loan

Fixed rate products shine in specific situations:

Funding one big expense. Adding a second story? Replacing your roof? Paying medical bills or writing a tuition check? These require known amounts upfront. Borrowing exactly what you need at a locked rate prevents over-leveraging. My uncle financed a $60,000 in-law suite addition this way—the fixed payment integrates cleanly with his pension and Social Security checks.

When rates are elevated or climbing. If the Fed's signaling more tightening or inflation stays stubborn, locking today protects you from tomorrow's increases. Plenty of 2026 borrowers view current fixed pricing as a ceiling rather than a floor, given how aggressive the tightening cycle's been.

You really value predictability. Living on retirement income? Single-earner household? Anxious about budget swings? Knowing your complete housing expense—original mortgage plus equity loan—never changes makes planning simpler and reduces financial stress.

Consolidating expensive debt with a clear finish line. Roll credit cards or personal loans charging 20%+ into a 7% fixed equity loan and you'll save upward of $500 monthly in interest on typical balances. The fixed term enforces discipline—you'll be completely debt-free in 10 or 15 years, unlike revolving accounts that can linger indefinitely.

Author: Hannah Whitlock;

Source: isomfence.com

Skip fixed products when:

- You need capital sporadically over several years (a line of credit handles this better) - You're confident rates will drop substantially and want automatic savings without refinancing hassle - You might sell within three years—recouping closing costs or navigating early-payoff penalties gets messy

How to Qualify and Apply

Because these loans sit behind your first mortgage in foreclosure priority, lenders scrutinize applications harder.

Credit minimums: Most require 660, though hitting 680+ unlocks noticeably better pricing. Expect a hard inquiry that temporarily dings your score 5–10 points. Recent delinquencies, collection accounts, or bankruptcies within 24 months usually trigger automatic denial or require extensive documentation.

Proving your income: Gather recent pay stubs, last year's W-2s, or complete tax returns if you're self-employed (Schedule C plus full 1040s for two years). Underwriters divide all your monthly debt payments—existing loans plus the proposed equity loan—by gross monthly income. Push past 43% and you're likely getting rejected. Stay under 36% and you're in good shape.

Property appraisal: Lenders order full appraisals to nail down current value, typically costing $400–$700. Appraisers tour your home, analyze recent neighborhood sales, and deliver findings within 7–10 days. If the valuation lands below your estimate, your borrowing power shrinks. Example: you think your home's worth $400,000 and want $60,000 at 80% CLTV. But the appraisal comes back at $380,000. With your existing $250,000 mortgage, your maximum new loan drops to $54,000.

Typical closing costs: Budget 2–5% of your loan amount. That $50,000 loan might generate $1,000–$2,500 in fees: origination charges (0.5–1% of loan), title examination ($300–$500), recording costs ($50–$200), plus that appraisal. Some lenders advertise no-closing-cost loans by either rolling fees into your principal or bumping your rate slightly.

Author: Hannah Whitlock;

Source: isomfence.com

How long it takes: Plan on 3–6 weeks from application to funding. Here's the usual sequence:

1. Initial qualification (1–2 days): Soft credit check and preliminary income review

2. Full application (1 day): Submit complete documentation package

3. Appraisal (7–14 days): Schedule and complete property inspection

4. Underwriting (5–10 days): Lender verifies credit, income, title status

5. Closing (1 day plus 3-day rescission): Sign documents; federal law delays fund release three business days

Common mistakes:

- Overestimating home value: Online tools miss the mark by 10% or more frequently. Check actual recent sales in your neighborhood for realistic expectations. - Ignoring debt-to-income limits: Adding a $500 equity payment when you're already at 40% DTI might push you over lender thresholds. - Assuming rates are locked: Quotes can shift between application and closing. Get written rate-lock confirmation with specific expiration dates.

Frequently Asked Questions About Fixed Rate Home Equity Loans

A fixed rate home equity loan gives you straightforward access to your property's accumulated value while delivering payment stability that adjustable alternatives can't match. Receiving your full loan amount upfront with a permanently locked rate provides budget certainty and protection from future rate escalation—benefits that prove especially valuable during sustained high-rate periods or when funding essential expenses like healthcare or education.

Choosing between fixed versus variable home equity structures demands honest assessment of your comfort with uncertainty, your spending pattern, and your rate forecast. Value predictability? Need a single lump sum? Expect rates to stay elevated or climb? Fixed borrowing aligns perfectly. Prefer maximum flexibility and believe rates will decline meaningfully? An adjustable line might suit you better.

Before applying, confirm your credit standing, estimate your property's current worth using actual recent neighborhood sales, and calculate your anticipated post-loan debt-to-income ratio to verify affordability. Request quotes from at least three lenders to compare pricing, fee structures, and prepayment policies—seemingly small differences compound significantly over 15-year terms. Armed with thorough knowledge of how fixed home equity rates work, you can tap your home's value with confidence and genuine cost efficiency.

Related Stories

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to home loans, mortgage rates, home equity loans, and the home buying process.

All information, including articles, guides, and explanations, is provided for general educational purposes only. Mortgage terms, interest rates, eligibility requirements, and lending conditions may vary depending on individual financial situations, lenders, and regional regulations.

This website does not provide financial, legal, or mortgage advice, and the information presented should not be considered a substitute for consultation with qualified financial professionals, lenders, or advisors.

The website and its authors are not responsible for any errors or omissions, or for any decisions made based on the information provided on this website.