Homebuyer reviewing mortgage documents at a desk

How Much Home Loan Can I Get Based on My Income

Shopping for a house means answering one big question first: what will a bank actually let you borrow? That number might surprise you—sometimes in good ways, sometimes not. I've seen buyers with identical $85,000 salaries walk away with wildly different approval amounts. One gets $400,000, another caps out at $280,000, and a third gets turned down completely.

Why? Banks assess your entire financial picture before deciding how lenders size a home loan for you. Your paycheck matters, obviously. But so do your car payment, credit card balances, student loans, savings account, credit history, and even how long you've worked at your current job. Miss one detail and you might lose $50,000 in buying power without realizing it.

Here's what most first-time buyers don't grasp: lenders follow strict formulas, but those formulas have wiggle room. Learn the rules and you can maximize your approval amount. Ignore them and you'll either borrow less than you could have or—worse—get denied after making an offer.

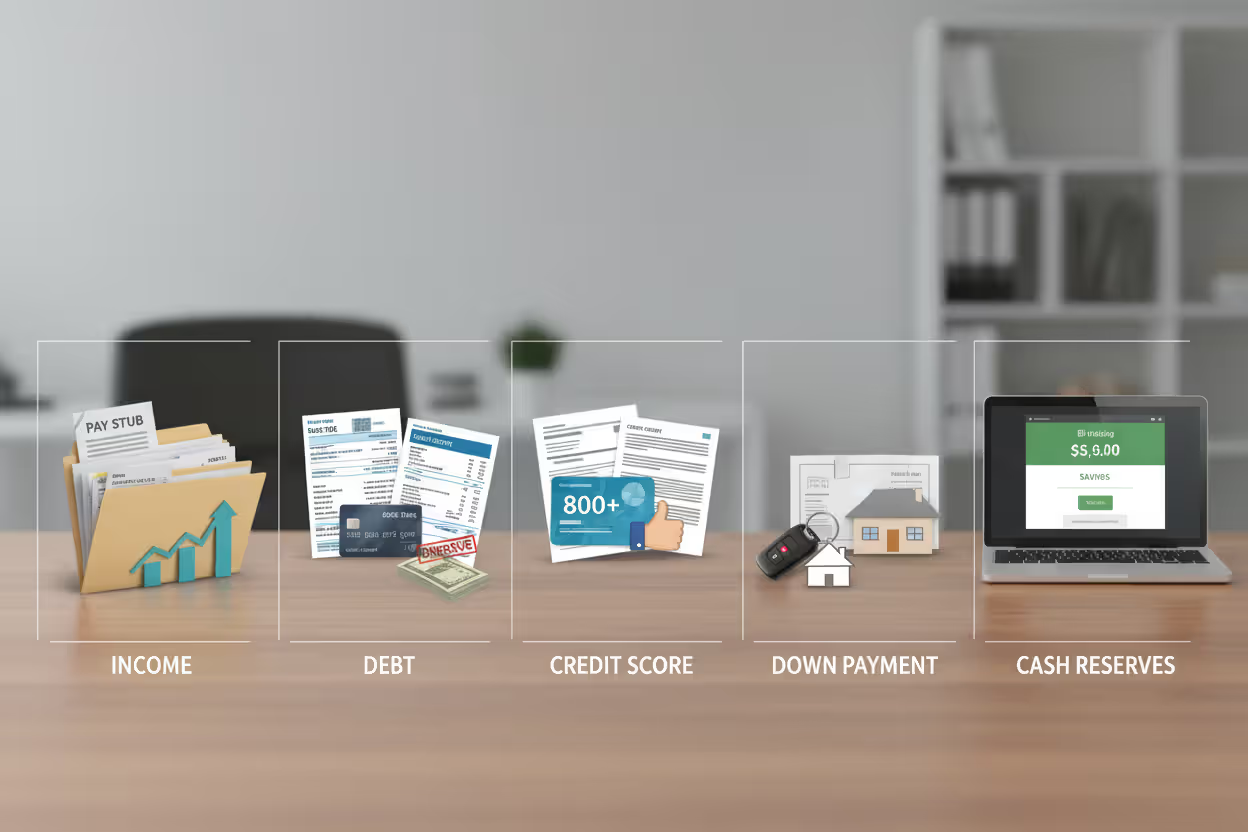

What Lenders Look at When Sizing Your Home Loan

Banks examine five major pieces of your financial life before deciding your home loan borrowing limit:

Author: Ethan Callahan;

Source: isomfence.com

Your income—and proof it'll continue. Banks prefer borrowers who've earned steady paychecks from the same employer for years. A nurse making $75,000 annually at the same hospital for three years looks safer than a consultant who invoiced $110,000 last year but $60,000 the year before. Stability beats higher numbers if the higher numbers bounce around.

Your debt load compared to earnings. Banks add up everything you owe monthly—car payment, student loans, credit cards, child support—then compare that total to your monthly income. This ratio determines whether you're overextended or have room to take on a mortgage. A $5,000 monthly salary looks great until the bank sees you're already sending $2,200 to other creditors every month.

Your credit history and score. Poor credit doesn't just mean higher interest rates. It can block approval entirely or force you into programs with lower maximum loan amounts. FHA loans accept 580 scores if you put down 3.5%, but you'll need 620 minimum for most conventional mortgages. Hit 740 and you unlock the best terms and highest lending limits.

Cash you're putting down. The more skin you have in the game, the more banks will lend you. Put down 3% and you're capped by stricter rules. Put down 20% and you avoid mortgage insurance, which frees up hundreds of dollars monthly that can go toward a bigger loan payment instead.

Reserves in the bank after closing. Lenders don't want you scraping by. They check that you'll have cushion left after paying your down payment and closing costs—usually two to six months' worth of mortgage payments sitting in savings. Drain your accounts to maximize your down payment and you might actually hurt your approval odds.

Different lenders weight these factors differently, which is why shopping around matters. One credit union might stretch on income verification for longtime members. Another bank might rigidly follow automated underwriting rules with zero flexibility.

How to Calculate Your Maximum Home Loan Amount

Most lenders lean on the 28/36 guideline, though it's not universal anymore. The first number means your housing costs—mortgage, property tax, homeowners insurance, and HOA fees if applicable—shouldn't eat up more than 28% of your monthly gross pay. The second number caps your total debt obligations, including that housing payment, at 36% of what you earn monthly before taxes.

Here's the math for the housing-only limit:

- Take your yearly salary and divide by 12 to get monthly gross income

- Multiply that monthly figure by 0.28

- The result shows your maximum monthly housing budget under this rule

Let's say you earn $75,000 annually: $75,000 ÷ 12 gives you $6,250 monthly. Multiply $6,250 by 0.28 and you get $1,750 as your housing payment ceiling.

Now calculate the back-end limit that includes all your debts:

- Take that same monthly gross income and multiply by 0.36

- Add up what you currently pay monthly toward cars, students loans, credit cards, and personal loans

- Subtract your current debts from the 0.36 figure—what remains is available for housing

Using our $75,000 example again: $6,250 times 0.36 equals $2,250 in total allowable monthly debt. If you're already paying $400 for a car and $150 toward student loans, that's $550 going out the door. Subtract $550 from $2,250 and you've got $1,700 left for your mortgage payment.

The tighter of these two calculations determines your real limit. In this scenario, the 36% rule restricts you to $1,700 monthly, not the $1,750 the 28% rule would allow.

Converting a monthly payment into an actual loan amount requires factoring in current interest rates, estimated property taxes, insurance premiums, and any HOA dues. At 6.5% interest with $250 monthly property tax and $100 insurance, that $1,700 payment might support roughly a $265,000 mortgage.

Author: Ethan Callahan;

Source: isomfence.com

Maximum Home Loan Amount by Annual Income and DTI Ratio

| Annual Income | 28% DTI Monthly Max | 36% DTI Monthly Max | 43% DTI Monthly Max | Estimated Loan at 36%* |

| $50,000 | $1,167 | $1,500 | $1,792 | $210,000 |

| $75,000 | $1,750 | $2,250 | $2,688 | $330,000 |

| $100,000 | $2,333 | $3,000 | $3,583 | $450,000 |

| $125,000 | $2,917 | $3,750 | $4,479 | $570,000 |

| $150,000 | $3,500 | $4,500 | $5,375 | $690,000 |

*Calculations assume 6.5% rate, $300 monthly for taxes and insurance combined, no homeowners association fees, zero existing debt, 20% down payment.

Remember that plenty of lenders now approve borrowers at 43% or even 50% debt ratios if you bring excellent credit, big cash reserves, or qualify for specific programs. This table shows what monthly payments look like at different thresholds—your actual maximum home loan based on income will depend on your complete financial snapshot.

Author: Ethan Callahan;

Source: isomfence.com

Income Types That Count Toward Home Loan Eligibility

Lenders treat income sources differently. The unifying requirement: your earnings must be stable, properly documented, and reasonably expected to continue at least three years.

Traditional W-2 employment makes underwriters happiest. They verify using your recent pay stubs, last two years of W-2 forms, and sometimes a quick phone call to your HR department. Two-plus years at your current job and you're golden.

Running your own business means more paperwork. Expect to hand over two full years of personal tax returns plus two years of business returns—1120s, 1120-S forms, or 1065s if you've got partners. Lenders calculate an average of your net profit across those two years. If your Schedule C showed $80,000 one year and $70,000 the previous year, they'll use $75,000 as qualifying income. Year-over-year declines can trigger denials.

Commissions and bonuses only help if you've received them consistently for 24 months. That one-time $10,000 signing bonus? Doesn't count. But quarterly commission checks that show up on your W-2 for two years straight get averaged and added to your base salary.

Regular overtime follows identical rules—two-year history showing consistent extra hours. If you've worked 10 overtime hours weekly for 24 months, lenders include that income. Occasional overtime gets ignored.

Alimony and child support work if you can document at least three years of future payments remaining. You'll provide your divorce decree plus bank statements proving you actually receive the payments on schedule.

Rental property income counts at a discount. Lenders typically use 75% of gross rent to account for vacancies and repairs. Collect $2,000 monthly and they'll credit you with $1,500. You'll need signed leases and tax returns showing the rental income.

Social Security and pension income both count at full value if they're permanent. Disability payments qualify too, provided they don't expire within three years.

Part-time work qualifies after two years of history. A teacher working full-time who also tutors evenings can use both income sources if the tutoring has continued for 24 months.

Author: Ethan Callahan;

Source: isomfence.com

How Lenders Verify and Average Your Income

W-2 employees face straightforward verification: your two most recent pay stubs, W-2 forms from the past two years, and employment confirmation directly from your employer. Lenders calculate monthly income by examining your year-to-date earnings on your most recent pay stub and projecting that forward.

Self-employed borrowers endure tougher scrutiny. You'll produce two years of complete personal tax returns plus two years of business returns. The underwriter adds back non-cash expenses like depreciation but subtracts business costs, health insurance you deducted, and your self-employment tax adjustment.

Own 25% or more of any business? You're self-employed even if that business issues you a W-2. This triggers the intensive documentation requirements.

Here's a trap: self-employed buyers often write off maximum expenses to minimize tax bills, then discover their documented income falls short of what they need for their target mortgage. Planning to buy within two years? Talk to your CPA about balancing tax savings against home loan amount eligibility.

How Your Debt-to-Income Ratio Affects Borrowing Limits

This ratio frequently becomes the limiting factor on how much you can borrow. Banks calculate it by totaling your monthly debt obligations and dividing by your gross monthly income.

Count these obligations:

- Your future mortgage payment including principal, interest, property tax, and insurance

- Auto loans and lease payments

- Student loans—even deferred ones, using either the actual payment or 0.5% to 1% of your balance

- Credit card minimums based on your current reported balances, not what you typically pay

- Personal installment loans

- Child support and alimony you're obligated to pay

- Co-signed loans unless you prove someone else has made all payments for over a year

Exclude these:

- Utility bills, cell phone service, and car insurance

- Groceries, gas, and other variable expenses

- Medical bills unless they've gone to collections

- Debts with under 10 payment remaining (some lenders)

Conventional loans typically max out at 43%, though Fannie Mae and Freddie Mac stretch to 50% for borrowers with credit scores above 700 and solid reserves. FHA loans officially cap at 43% but can reach 50% or higher with strong compensating factors like substantial down payments or perfect payment histories.

Author: Ethan Callahan;

Source: isomfence.com

Strategies for improving your ratio before applying:

Pay credit cards down below 30% utilization—this helps your score while reducing monthly minimums. Got a car loan with 10 months left? Pay it off completely. Eliminating that $400 monthly obligation could boost your buying power by $60,000 to $80,000.

Don't open new accounts. That furniture store financing or new car lease immediately reduces your available borrowing capacity. Refinancing student loans to lower payments can help, but do it six months before your mortgage application—recent credit inquiries and new tradelines complicate underwriting.

Sitting near a ratio threshold? Ask your lender about a slightly smaller loan amount that brings you under the limit, then increase your down payment to reach your target purchase price.

Other Factors That Determine Your Home Loan Limit

Income and debt ratios aren't the whole story. Several other variables affect your borrowing ceiling.

Minimum credit scores vary by program:

- FHA: 580 for 3.5% down; 500-579 requires 10% down

- VA: no hard floor, but most lenders want 620 or better

- USDA: 640 minimum for automated approvals

- Conventional: 620 to get approved; 740+ unlocks best pricing

Someone with a 640 score might get approved for less than an applicant with a 760 score despite identical income. Lower scores trigger higher rates, which inflates monthly payments and shrinks how much house you can afford.

Your down payment percentage carries more weight than buyers realize. Come in with 5% down and you'll pay PMI—typically $100 to $300 monthly depending on your score and loan size. That insurance premium consumes part of your debt ratio capacity. Put down 20% and PMI disappears, freeing up room in your budget for a larger mortgage.

Loan program choice creates different ceilings. FHA loans cap borrowing at county limits—$498,257 in most counties for 2026, higher in expensive markets. Conventional conforming loans hit $806,500 (2026 baseline), with higher limits in costly areas. VA loans technically have no ceiling, but your income and ratios still restrict what you can borrow. Jumbo loans exceeding conforming limits demand stronger credit, lower ratios, and larger reserves.

Where you're buying matters more than you'd think. A $500,000 mortgage is conforming in San Francisco but jumbo in rural Kansas. Jumbo programs typically require 700+ scores, 10%-20% down, and ratios below 43%—all of which can reduce your maximum borrowing power even when your income could theoretically support more.

Recent job changes raise questions. Switch employers within the past few months? Expect to provide an offer letter or employment contract and explain why you moved. Gaps exceeding 30 days between jobs require written explanations. Lenders prefer two years in the same position, but they'll accept job changes within your industry if income remained steady or increased.

Common Mistakes That Reduce Your Borrowing Power

Author: Ethan Callahan;

Source: isomfence.com

Opening new credit between pre-approval and closing destroys more deals than almost anything else. You get pre-approved for $400,000, then finance $35,000 in furniture and a $50,000 truck before closing. The lender runs your credit again three days before you're supposed to sign papers, sees your ratios have exploded, and pulls your approval. The sale collapses. Never apply for credit cards, finance purchases, or even let furniture stores run your credit between initial approval and closing day.

Forgetting property taxes and insurance in your calculations creates ugly surprises. First-timers often calculate affordability using only principal and interest, forgetting property taxes might add $400 monthly and insurance another $150. In high-tax states like Texas or New Jersey, that $2,000 monthly budget might only support a $250,000 loan instead of the $320,000 you assumed.

Self-employed borrowers overestimating qualifying income happens constantly. You generated $200,000 in gross business revenue, but after legitimate deductions your tax return shows $85,000 net profit. Lenders use that $85,000 figure, not $200,000.

Discovering credit problems during your application kills deals. You apply and find out about a $1,200 medical collection from three years ago. That single item can drop your score 40 points and flip you from approved to denied. Pull your credit reports from Equifax, Experian, and TransUnion six months before applying. Dispute errors, settle collections, and give your score time to recover.

Changing jobs right before applying creates unnecessary obstacles. Banks want employment stability. Thinking about switching careers? Either do it well before your mortgage application or wait until after you close. Moving from W-2 employment to self-employment is especially problematic—you'll typically need two full years of self-employment income before qualifying.

Draining savings to maximize your down payment can backfire badly. Lenders want reserves—usually two to six months of mortgage payments still sitting in your accounts after closing. Empty your savings putting 20% down and you might get denied despite the large down payment. Often you're better off with 10% down and healthy reserves than 20% down with nothing left.

Co-mingling gift funds creates documentation nightmares. Your parents gift you $20,000 for your down payment. You deposit it and immediately apply for a mortgage. The lender now needs a gift letter, proof the funds came from your parents' account, proof they deposited into your account, and evidence of where your parents got the money. Large unexplained deposits trigger investigations that delay or kill approvals. Document everything carefully.

Buyers constantly confuse pre-qualification with pre-approval—that's the mistake that costs them houses.Pre-qualification is just me estimating what you might afford based on what you tell me over the phone. Pre-approval means I've verified your income documents, pulled your actual credit, and reviewed your bank statements. I've watched buyers lose their dream homes because they thought they were approved when they'd only been pre-qualified. Get fully underwritten before you tour houses—it separates serious buyers from people wasting their own time and everyone else's

— Jennifer Morales

Frequently Asked Questions About Home Loan Amounts

Knowing exactly how much home loan you can get based on your income puts you in the driver's seat. You're not guessing or crossing your fingers—you understand your numbers before falling in love with any property.

Start by running ratio calculations with different loan amounts. Online calculators give you ballpark estimates, but verify results with an actual lender who can evaluate your specific situation. Get pre-approved, not just pre-qualified, so you know your precise borrowing limit. This prevents heartbreak when you find the perfect house but can't finance it.

Treat your approved loan limit as a ceiling, not a target. Just because a bank approves you for $450,000 doesn't mean borrowing that much makes sense. Leave breathing room in your budget for repairs, maintenance, furniture, and life's inevitable surprises. Smart rule: if the monthly payment feels tight when you run the numbers, it'll feel crushing when you're actually living with it.

Time your application strategically. Self-employed? Apply after filing two years of tax returns showing strong, stable earnings. Paying off a car loan? Wait until it's gone before applying—your ratio will look dramatically better. Sitting at a 680 credit score? Spend six months pushing it to 720 before you apply. The improved rate could save you $200 monthly and increase your buying power by $40,000.

Finally, talk to multiple lenders. Ratio requirements, credit overlays, and documentation standards vary significantly. One lender might cap you at $350,000 while another approves $380,000 using identical financial information. Get loan estimates from at least three different lenders and compare maximum loan amounts alongside rates and total costs. The extra effort might mean the difference between compromising on a smaller house and getting exactly what you want.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to home loans, mortgage rates, home equity loans, and the home buying process.

All information, including articles, guides, and explanations, is provided for general educational purposes only. Mortgage terms, interest rates, eligibility requirements, and lending conditions may vary depending on individual financial situations, lenders, and regional regulations.

This website does not provide financial, legal, or mortgage advice, and the information presented should not be considered a substitute for consultation with qualified financial professionals, lenders, or advisors.

The website and its authors are not responsible for any errors or omissions, or for any decisions made based on the information provided on this website.