Person comparing mortgage offers with interest rate and APR documents at a desk

Home Loan APR Guide

When you're hunting for a mortgage, two numbers will jump out at you on every single offer: the interest rate and the APR. Here's the thing—most people zero in on that interest rate and call it a day. Big mistake.

The annual percentage rate? That's where the real story lives. It shows you what you'll actually pay to borrow money for your home, not just the glossy headline number lenders love to advertise.

Here's what I mean: you might see a lender shouting about their amazing 6.5% rate. Sounds great, right? But then you notice they're charging $4,000 in origination fees, another $3,500 for discount points, plus mortgage insurance premiums. Suddenly that 6.5% becomes 6.875% APR. Those extra fees? They add up to thousands over the life of your loan. Understanding both numbers—and why they'll never match—can save you serious money.

What Is APR on a Home Loan?

Think of APR as your loan's "all-in" cost. It takes your base interest rate and rolls in specific fees required to actually get the loan. Your interest rate only tells you what you're paying on the amount you borrowed. APR adds origination charges, points, mortgage insurance, and other lender fees into the mix.

Federal law requires lenders to hand you this information within three business days of applying. You'll find it on your Loan Estimate—that standardized form exists specifically because lenders used to play games with fee structures, making apples-to-apples comparisons nearly impossible for regular borrowers.

When someone asks for apr on a home loan explained in simple terms, here's my go-to explanation: your interest rate is what you pay to borrow the bank's money. APR is what you pay to borrow it and set up the whole arrangement.

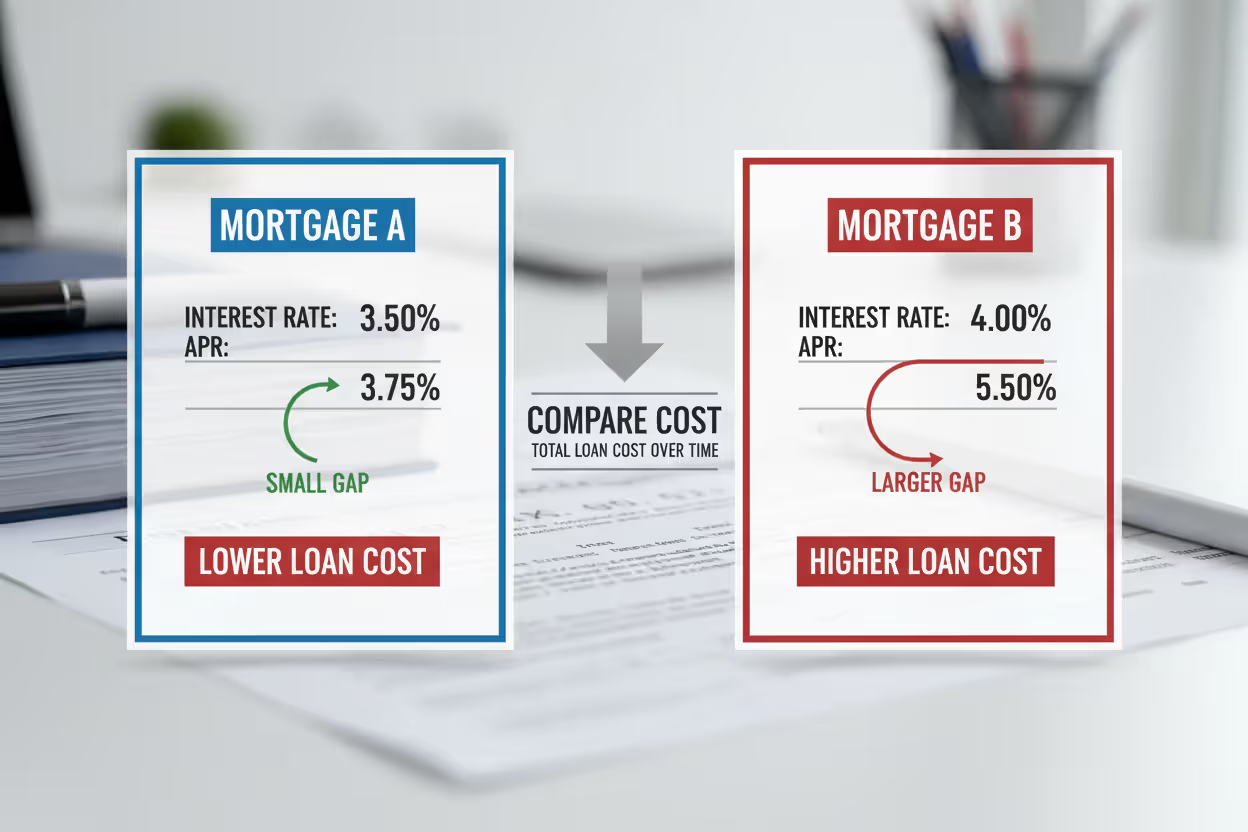

Let's say you're financing $300,000 at 6.5%. If your lender charges $3,000 in origination, you buy 1.5 points for $4,500, and you've got upfront mortgage insurance of $1,200, that 6.5% rate might actually cost you 6.82% APR. The difference between those two numbers? That's your fee load, expressed as a percentage.

A big gap means expensive fees. A narrow gap means the lender isn't hitting you as hard on closing costs.

Author: Ethan Callahan;

Source: isomfence.com

Interest Rate vs APR for Home Loans

Your interest rate determines your monthly payment. Period. Borrow $300,000 at 6.5% over 30 years, and you're looking at roughly $1,896 per month in principal and interest. Simple math based on your balance.

APR works differently. It takes those upfront costs, spreads them across your repayment schedule, and converts everything into a single percentage. That's why the interest rate versus apr for home loans matters so much when you're comparing offers with different fee structures.

Use each number for different purposes:

Check the interest rate when you're figuring out what you can afford monthly or whether a payment fits your budget.

Check the APR when you're comparing the total cost of similar loans from different lenders.

Your APR will always run higher than your interest rate—unless you stumble onto some unicorn scenario where the lender eats all closing costs. Usually, you're looking at a 0.125% to 0.5% difference on conventional loans. Though I've seen it exceed 1% when fees pile up or when buyers purchase multiple points.

| Feature | Interest Rate | APR |

| What's included | Just the cost of borrowing the principal | Interest rate plus origination fees, points, MI premiums, and other mandatory lender charges |

| What it tells you | The percentage charged on your loan balance | Your true yearly cost expressed as a percentage |

| When to use it | Calculating monthly payments and affordability | Comparing total costs between similar loan products |

| Typical difference | — | Usually 0.125% to 0.5% higher (sometimes more) |

One catch: APR assumes you'll keep the loan for its full term. Refinance after five years? That calculation doesn't reflect reality since you paid upfront fees for a 30-year loan you only kept for five.

Author: Ethan Callahan;

Source: isomfence.com

How Home Loan APR Is Calculated

Lenders use a formula that converts your upfront fees into an interest-rate equivalent, then combines it with your base rate. You won't need to crunch these numbers yourself—that's what their software does—but understanding the mechanics explains why APR diverges from your stated rate.

The how home loan apr is calculated process starts with these inputs:

Loan amount: What you're actually borrowing, not your home's purchase price.

Interest rate: Your base rate before any fees get factored in.

Loan term: Could be 15 years, 30 years, or something else entirely.

Finance charges: The lender's required fees to close your loan (detailed in the next section).

Here's a real-world example:

You're financing $350,000 at 6.75% over 30 years. Your lender charges 1% origination ($3,500), you're buying 1 point to lower your rate ($3,500), and upfront MI costs $1,750. Total finance charges: $8,750.

To calculate APR, the lender figures out what interest rate on $341,250 (your $350,000 minus the $8,750 in fees) would create the same monthly payment as 6.75% on the full $350,000. Run the math, and you'll land somewhere around 7.05% APR.

This involves solving for rate in a present-value equation—exactly why lenders rely on specialized software. The key takeaway? Bigger fees relative to your loan amount create a wider spread between rate and APR.

Smaller loans amplify this effect. Finance that same $150,000 with the same $8,750 in fees, and your APR jumps to about 7.35% because those charges represent a much larger chunk of your principal.

Author: Ethan Callahan;

Source: isomfence.com

What Fees Are Included in APR?

Not every closing cost factors into APR. Only charges paid directly to your lender—or required by your lender for loan approval—make the cut. Third-party costs you'd face regardless of which lender you pick typically stay out of the calculation.

What's included in APR:

- Origination fees: Processing and underwriting charges, typically 0.5% to 1% of your loan amount

- Discount points: Upfront payments that buy down your rate—each point equals 1% of your principal

- Broker fees: Compensation paid to mortgage brokers if you're using one

- Upfront mortgage insurance: The initial premium on FHA loans or the first portion of PMI

- Prepaid interest: Interest that accrues between your closing date and first payment

- Lender-required fees: Things like underwriting charges, document prep, and rate lock fees

What's excluded from APR:

- Appraisal fees: You'll pay for a property valuation no matter which lender you choose

- Credit report costs: The expense of pulling your credit

- Title services: Title insurance and searches needed for any transaction

- Attorney fees: Closing lawyer costs

- Homeowners insurance: Your annual policy premium

- Property taxes: Local government charges that have nothing to do with your loan

- HOA fees: Community association dues

- Recording fees: Government charges to record your deed

Understanding apr charges on home loans means recognizing these distinctions. When lenders advertise "no closing costs," they usually mean their fees, not third-party expenses. You'll still pay for appraisal, title work, and similar services.

Some lenders inflate third-party cost estimates on Loan Estimates to make their APR look better—then actual costs come in lower. Others underestimate. Don't fixate on APR alone. Dig into the detailed fee breakdown on page 2 of your Loan Estimate.

Author: Ethan Callahan;

Source: isomfence.com

How to Use APR When Comparing Home Loans

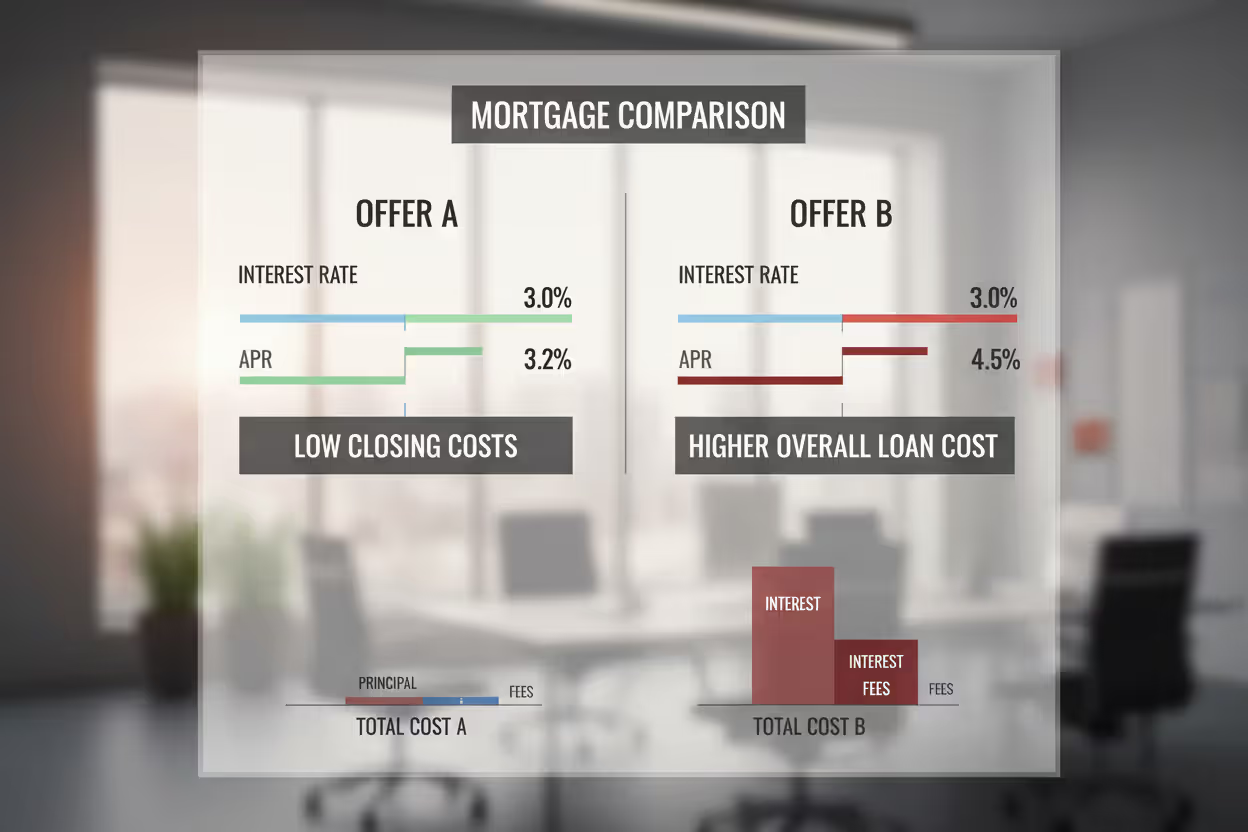

Want a practical home loan annual percentage rate guide? Get Loan Estimates from at least three lenders for identical loan amounts, types, and terms. Then line up the APRs side by side.

Say Lender A quotes 6.5% with a 6.75% APR. Lender B offers 6.625% with a 6.70% APR. Even though Lender B's interest rate is higher, they're actually cheaper overall—that lower APR reveals more reasonable fees.

This strategy works best when you're comparing: - The same loan type (conventional to conventional, FHA to FHA) - Identical terms (30-year to 30-year) - The same loan amount - Quotes pulled on the same day or within a few days (rates move constantly)

APR comparison breaks down in these scenarios:

Different loan terms: A 15-year mortgage always shows a lower APR than a 30-year loan at the same rate and fees—upfront costs get spread across fewer, larger payments. Never compare 15-year APRs to 30-year APRs.

Adjustable-rate mortgages: ARM APRs rely on assumptions about future rate adjustments that might prove totally wrong. That 5/1 ARM's APR assumes rates will adjust based on today's index values for the full 30 years.

Short-term ownership plans: Planning to sell or refinance in three years? A loan with high fees and a low rate might cost you more than the APR suggests because you're paying upfront for savings you'll never collect.

Different loan types: Comparing an FHA loan's APR to a conventional loan's APR is like comparing apples to oranges. FHA mortgages include ongoing mortgage insurance premiums that conventional loans can avoid with 20% down.

APR gives you useful information, but it shouldn't be your only deciding factor. I've seen borrowers chase the lowest APR and end up spending more because they refinanced two years later. Your best loan depends on your situation—how long you'll keep it, how much cash you have for closing, whether you value lower payments over lower total cost

— Michael Harrison

Common Mistakes When Evaluating Home Loan APR

Choosing based on APR alone: Some borrowers automatically pick the lowest APR without considering whether they can actually afford the monthly payment. Sure, 6.5% with a 6.9% APR beats 6.75% with a 6.95% APR on paper—but if that first option requires buying three points upfront, can you swing the payment difference?

Ignoring how long you'll keep the loan: Most homeowners move or refinance within seven years. Spending $6,000 on discount points to shave your rate only makes sense if you keep the mortgage long enough for monthly savings to exceed that initial cost. APR calculations assume you'll keep it for 30 years.

Mixing loan types: FHA loan APRs include lifetime mortgage insurance (on loans with less than 10% down). Conventional loan APRs might only reflect PMI until you hit 20% equity. That FHA APR looks higher—but the loan could still cost less if your credit's imperfect.

Comparing different terms: You can't directly compare a 15-year mortgage at 6.25% with a 6.4% APR to a 30-year loan at 6.5% with a 6.7% APR. The shorter loan shows a lower APR partly because you're paying off debt faster, not necessarily because fees are cheaper.

Thinking APR captures everything: Property taxes, homeowners insurance, and HOA fees can add hundreds to your monthly payment—but they're invisible in APR. Two identical mortgages on different properties might have wildly different total monthly costs.

Comparing quotes from different days: Mortgage rates shift constantly. Getting one quote Monday and another Thursday? The difference might just reflect market movement, not better pricing.

Better approach: request Loan Estimates from multiple lenders on the same day for identical loan scenarios. Compare both APR and itemized fees. Factor in how long you'll realistically keep the loan.

Author: Ethan Callahan;

Source: isomfence.com

Frequently Asked Questions About Home Loan APR

APR works as a standardized tool for evaluating the true cost of different mortgage products—but it's got limitations. Understanding what APR includes, how it differs from your interest rate, and when comparisons fall apart puts you in a stronger position to assess your options.

Get Loan Estimates from several lenders. Compare APR figures and detailed fee lists. Factor in your realistic timeline. A mortgage with a slightly higher APR but lower upfront costs might serve you better if you'll probably refinance in three years. Conversely, paying more initially for a lower rate benefits long-term homeowners.

Your best mortgage isn't necessarily the one with the smallest APR—it's the one that fits your financial situation, timeline, and goals. Treat APR as one tool in your decision-making process, not the only one that matters.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to home loans, mortgage rates, home equity loans, and the home buying process.

All information, including articles, guides, and explanations, is provided for general educational purposes only. Mortgage terms, interest rates, eligibility requirements, and lending conditions may vary depending on individual financial situations, lenders, and regional regulations.

This website does not provide financial, legal, or mortgage advice, and the information presented should not be considered a substitute for consultation with qualified financial professionals, lenders, or advisors.

The website and its authors are not responsible for any errors or omissions, or for any decisions made based on the information provided on this website.