Top view of a desk with mortgage documents, stack of US dollar bills, house keys, and a small white house model representing a home buying financial decision

Discount Points Mortgage Guide

Most homebuyers get confused when their lender starts talking about paying extra money upfront to lower their interest rate. Should you really hand over several thousand dollars at closing just to shave a fraction off your mortgage rate? It depends—and getting this decision wrong can cost you serious money either way.

What Are Mortgage Discount Points?

Think of loan discount points as prepaying some of your mortgage interest before you even make your first monthly payment. Here's how the math typically works: you pay 1% of your total loan amount upfront, and your lender drops your interest rate by about 0.25%. That "about" matters, though. Some lenders might only give you a 0.20% reduction. Others might go as high as 0.30%. Market conditions, your credit score, and how badly lenders want your business all play a role.

Let's make this concrete with mortgage points explained through a real scenario. You're borrowing $300,000. One discount point costs you $3,000 at the closing table. If that point brings your rate down from 6.5% to 6.25%, you'll pay less interest every single month. But you need to keep that mortgage long enough to actually recover that three grand you spent upfront.

Now here's something that trips people up constantly: origination points versus discount points. They're completely different animals. Origination points? That's just the lender charging you to process your paperwork—essentially their fee for doing their job. Discount points actually buy you something valuable: a lower interest rate for the life of your loan. Some lenders will quote you "2 points" without clarifying whether that's 1 origination + 1 discount, or 2 discount points, or what. Don't let them get away with vague answers. Demand an itemized breakdown showing exactly what you're paying for and what you're getting in return.

Author: Ethan Callahan;

Source: isomfence.com

That quarter-point reduction isn't carved in stone, either. During my research for this article, I found lenders offering anywhere from 0.15% to 0.35% per point, depending on market volatility. When rates are jumping around, lenders get conservative and might only offer 0.20% reductions. In stable, competitive markets, they'll sometimes go higher to win your business.

How Mortgage Points Work When Buying Down Your Interest Rate

The mortgage rate buy down process starts when you apply. Your loan officer presents you with options: here's your rate with zero points, here's the rate if you buy one point, here's what happens with two points. They're essentially showing you different price points for the same product.

What's actually happening behind the scenes? Lenders calculate how much profit they need from your loan. When you pay discount points, you're giving them that profit upfront instead of spreading it across 30 years of interest payments. They're happy because they get cash now. You benefit because you lock in lower monthly costs. Win-win—assuming you keep the loan long enough.

The buying down interest rate evaluation follows a predictable path, though most people skip crucial steps:

First, collect rate quotes showing various point scenarios. Second, calculate actual dollar savings per month for each option. Third—and this is where people mess up—make an honest assessment of how long you'll realistically keep this loan. Fourth, determine if you'll hit break-even before you refinance or sell. Fifth, decide whether tying up that cash makes sense given everything else competing for your money.

Most lenders sell points in standard packages: zero, one, one-and-a-half, two, sometimes more. Each tier shows you the interest rate and payment adjustment. Some lenders let you buy fractional amounts—like 0.75 points—for more customization, but many stick to half-point increments.

Example Calculation: Buying Down Your Rate

Let's run real numbers on a $400,000 mortgage over 30 years. Your lender offers 6.75% with no points, 6.50% if you buy one point, or 6.25% with two points.

Buying zero points: You'll pay $2,594 monthly for principal and interest. Nothing extra at closing for rate reduction.

Buying one point ($4,000 upfront): Monthly payment drops to $2,527. You're saving $67 every month. How long until that $4,000 investment pays off? Divide $4,000 by $67, and you get roughly 60 months—that's five years. Keep the loan for the full 30 years, and you'll save about $20,120 in interest. Subtract your $4,000 cost, and you're ahead by $16,120.

Author: Ethan Callahan;

Source: isomfence.com

Buying two points ($8,000 upfront): Payment falls to $2,461 monthly. That's $133 less than the no-point option. Again, you hit break-even around month 60. Over three decades, you net approximately $31,880 after subtracting the $8,000 initial investment.

But wait—what if you sell after three years? You paid $8,000 for two points but only saved $133 × 36 months = $4,788. You just lost $3,212 on that bet.

The loan size factor matters enormously. A $150,000 mortgage might only save you $35 monthly with one point purchased. Meanwhile, a $900,000 jumbo loan could save you $165 per month from the same rate reduction. Bigger loans make points more attractive because the absolute dollar savings scale up.

How Much Do Mortgage Discount Points Cost?

The pricing formula stays consistent: one point equals exactly 1% of whatever you're borrowing. Mortgage points cost calculation is straightforward multiplication. Borrowing $250,000? Each point runs $2,500. Taking out $750,000? You'll pay $7,500 per point. The percentage never changes—just the dollar amount.

What does change is how much value you extract from each point. Your credit score makes a huge difference. Someone with a 780 score typically gets better rate reductions per point than someone at 680. Put 20% down instead of 5%? Your points might work harder for you. Conventional loans often deliver better point economics than FHA or VA loans, though government-backed programs have other advantages.

Geography plays a minor role. Cities with ten competing lenders might offer slightly better point pricing than rural areas with limited options. We're talking small differences though—maybe 0.03% to 0.05% variation in what each point buys you.

The overall rate environment reshapes point economics dramatically. When rates are high, points deliver bigger absolute savings. Dropping from 7.5% to 7.25% saves you more monthly dollars than reducing 4.5% to 4.25%, even though both are identical percentage drops. Higher baseline rates mean each quarter-point reduction affects a larger interest calculation.

Watch out for diminishing returns. Some lenders structure point pricing so your first point gives you 0.25%, the second delivers only 0.20%, and a third (if they even allow it) might only knock off 0.15%. They're basically telling you "we'll give you a deal on the first one, but don't get greedy."

One ironclad rule: you absolutely must pay for points with cash at closing. Financing the cost of points defeats the entire purpose. You'd be paying interest on the money you borrowed to reduce your interest rate. That's like using a credit card to pay off a credit card. The math just doesn't work.

When Buying Discount Points Makes Financial Sense

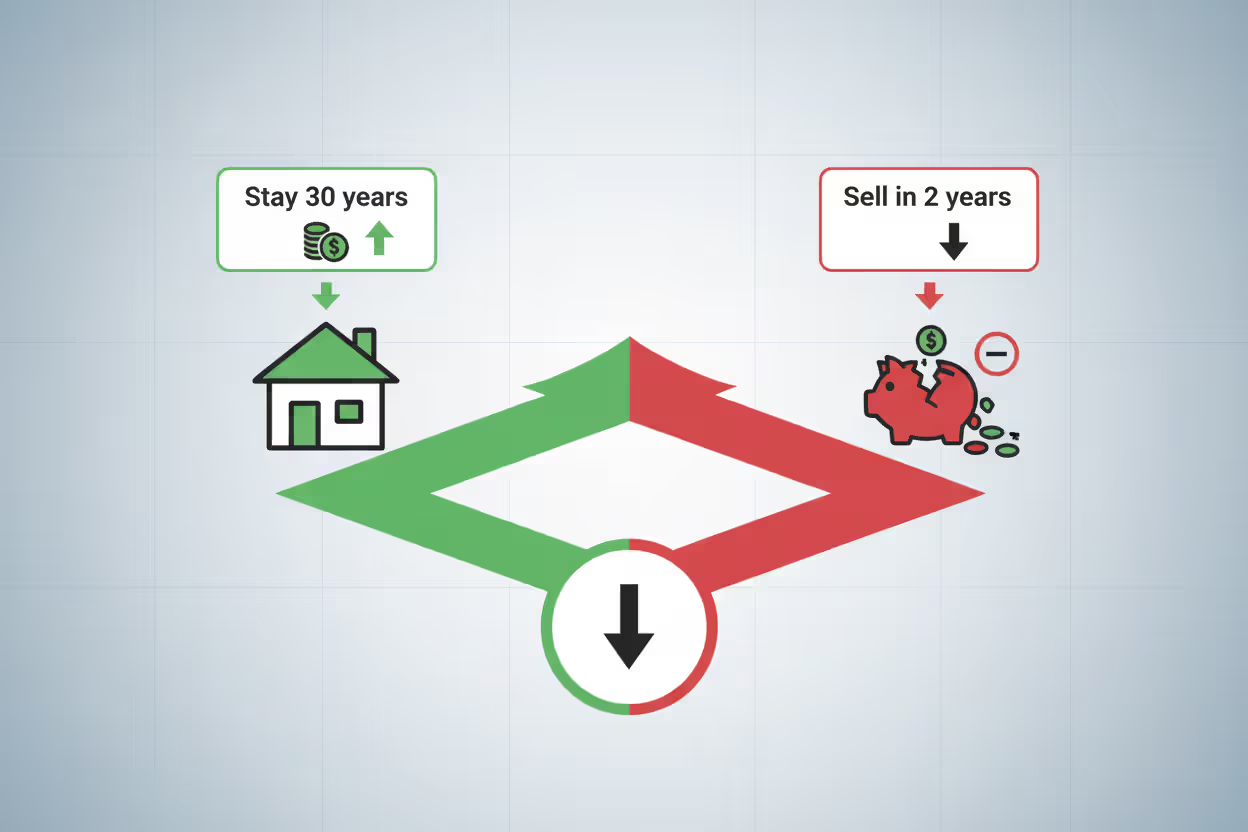

Loan duration expectations dominate everything else. Planning to stay put for 10+ years? Points probably make sense. Thinking you might relocate within five years? Skip them.

Cash availability matters just as much. Are you draining your emergency fund to buy points? Bad idea. Passing up better investment opportunities? Also questionable. Points make sense when you've got excess cash beyond your six-month emergency reserve and you're not sacrificing higher-return alternatives.

Author: Ethan Callahan;

Source: isomfence.com

Your tax situation influences the calculus. High earners who itemize and max out mortgage interest deductions get more mileage from points than people taking the standard deduction. The interest savings mean more when you're already optimizing mortgage interest for tax purposes.

Market timing creates interesting scenarios. Rising rate environments make locking in lower rates through points extra appealing. You're essentially buying insurance against future increases. Conversely, if you think rates will fall and you'll refinance soon, points become a waste.

Consider points when you're right on the edge of qualifying. Sometimes dropping your monthly payment by $100 makes the difference between approval and rejection. Just make sure adding $5,000 to your closing costs doesn't create a different problem.

Skip points entirely when refinancing seems likely within five years. Most break-even timelines stretch beyond 60 months, so you're gambling on loan duration. Also skip them when there's any decent chance you'll sell the property in the next several years.

Points deliver questionable value on adjustable-rate mortgages. You're only reducing the initial fixed period rate. Unless you're certain about refinancing before the adjustment hits, you're not getting full value.

Break-Even Point Calculator Explained

Your break-even calculation tells you exactly when accumulated monthly savings equal what you paid upfront. The basic math: divide total point cost by monthly payment reduction.

Using our earlier example: $4,000 cost ÷ $67 monthly savings = 59.7 months. After month 60, you've recovered your investment. Everything beyond that point is pure profit.

But this simplified calculation ignores opportunity cost—arguably the most important factor. That $4,000 could be earning returns elsewhere. Let's say you could realistically get 7% annually in an index fund. After five years, your $4,000 would grow to roughly $5,612. Sophisticated analysis compares your interest savings against realistic alternative investment performance.

More advanced calculations use present value formulas, discounting future savings back to today's dollars. This reveals whether points genuinely outperform your next-best financial opportunity. Most people skip this step, but it's the difference between making an informed decision and just guessing.

Break-even timelines across different loan amounts:

| Borrowed Amount | Single Point Cost | Monthly Savings (0.25% reduction) | Months to Break-Even |

| $200,000 | $2,000 | $29 | 69 |

| $300,000 | $3,000 | $43 | 70 |

| $400,000 | $4,000 | $58 | 69 |

| $500,000 | $5,000 | $72 | 69 |

| $750,000 | $7,500 | $108 | 69 |

Notice the consistency? Break-even periods hover around 58-72 months regardless of loan size, assuming standard quarter-point reductions. The proportion stays constant even as absolute dollars scale up.

Tax Implications and Other Considerations

The IRS generally allows you to deduct discount points in the year you pay them—but only on purchase loans, and only if you meet specific requirements. Points must be standard practice in your area, calculated as percentages of the loan, and the loan must be for buying or building your primary residence.

Refinance points follow different rules entirely. You can't deduct them all at once. Instead, you spread the deduction across the loan's full term. Pay $3,000 in refinance points on a 30-year mortgage? You can deduct $100 per year. That's a much weaker tax benefit than purchase loans offer.

The 2017 tax overhaul changed the game for many homeowners. Standard deductions jumped to $15,000 for single filers and $30,000 for married couples. Unless your itemized deductions—including mortgage interest, property taxes (capped at $10,000), and other qualifying expenses—exceed those thresholds, you won't itemize anyway. Point deductions become worthless in practical terms, even though you technically qualify.

Discount points increase your cash needs at closing. Already stretching to cover your down payment and standard closing costs? Adding $3,000 to $8,000 for points might be impractical or impossible. Some buyers assume seller concessions can cover points, but sellers typically resist paying for something that only benefits the buyer.

Refinancing possibilities demand careful thought. Buy points now, then refinance 18 months later when rates drop? You've essentially thrown that money away. Your new loan replaces the old one completely. Any unused point value simply vanishes.

While points don't increase your loan balance, they reduce available cash. That might force you to make a smaller down payment, potentially pushing you into a higher loan-to-value tier with worse baseline rates or requiring mortgage insurance you could have avoided.

Common Mistakes When Purchasing Discount Points

The single biggest error? Skipping break-even calculations entirely. People see a lower monthly payment and assume they're saving money without determining how long they need to keep the loan for those points to actually pay off. Always run the numbers before committing.

Ignoring opportunity cost ranks second. That $5,000 you're spending on points could be eliminating credit card debt at 18% interest, funding your 401(k) to capture employer matching, or building an investment portfolio. Points deliver a guaranteed return equal to your mortgage rate—currently 6-7% for many borrowers. That's decent, but not always your best option.

Author: Ethan Callahan;

Source: isomfence.com

Buying points on short-term mortgages wastes money. You're purchasing a starter home you'll outgrow in four years? You know you'll refinance when rates drop next year? Points make no sense. Your break-even timeline exceeds your realistic ownership period.

Some people buy points solely to qualify for the loan, reducing monthly payments just enough to satisfy debt-to-income requirements. This is risky. You're depleting your cash reserves to barely afford the home. What happens when the water heater dies or your car needs $2,000 in repairs?

Shopping failures cost borrowers thousands. Accepting your first lender's point pricing without comparing other options leaves money on the table. Lender A might reduce your rate by 0.25% per point while Lender B offers 0.30%. Over 30 years, that compounds significantly.

Fixating on points while ignoring other negotiable fees represents poor strategy. Sometimes negotiating away a $1,500 origination fee or securing $2,000 in lender credits provides better value than purchasing points. Look at the complete picture.

Confusing discount points with origination points leads to overpayment. A lender quotes you "a loan at one point" without clarifying what type. Is that a discount point that reduces your rate, or an origination point that's just a fee? Demand itemized pricing separating each component explicitly.

The biggest mistake I see is borrowers purchasing points without understanding their own timeline. If you're not confident you'll keep the loan for at least seven years, points are speculation rather than investment. The math only works when you capture the long-term savings

— Michael Rodriguez

Frequently Asked Questions About Mortgage Discount Points

Should you buy discount points? It completely depends on your specific situation. Run the break-even calculations. Be brutally honest about how long you'll keep the loan. Compare the guaranteed return against other uses for that cash. And avoid the common mistakes that turn a potentially smart strategy into an expensive lesson.

The best decision for someone planning to retire in their forever home differs dramatically from what makes sense for a professional expecting relocation in three years. Don't follow generic advice—perform calculations reflecting your actual circumstances.

Before committing to discount points, develop realistic homeownership timeline assessments, compare guaranteed returns against investment alternatives, and ensure upfront costs don't compromise financial stability. Points can save tens of thousands across a mortgage's lifespan, but only when employed strategically by borrowers who thoroughly understand both advantages and limitations.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to home loans, mortgage rates, home equity loans, and the home buying process.

All information, including articles, guides, and explanations, is provided for general educational purposes only. Mortgage terms, interest rates, eligibility requirements, and lending conditions may vary depending on individual financial situations, lenders, and regional regulations.

This website does not provide financial, legal, or mortgage advice, and the information presented should not be considered a substitute for consultation with qualified financial professionals, lenders, or advisors.

The website and its authors are not responsible for any errors or omissions, or for any decisions made based on the information provided on this website.