Top view of a wooden desk with mortgage documents, house keys, a small house model, and a pen in soft natural lighting

What Is PMI and How Does It Affect Your Mortgage

Shopping for your first home with less than 20% saved for a down payment? You'll probably run into PMI during the loan approval process. Those three letters can tack on an extra $100 to $400 to your monthly housing costs—and most buyers don't fully understand what they're paying for or how to ditch it once they've built up enough equity. Let's break down exactly what private mortgage insurance does, what you'll shell out for it, and the fastest ways to cancel it.

Private Mortgage Insurance Explained

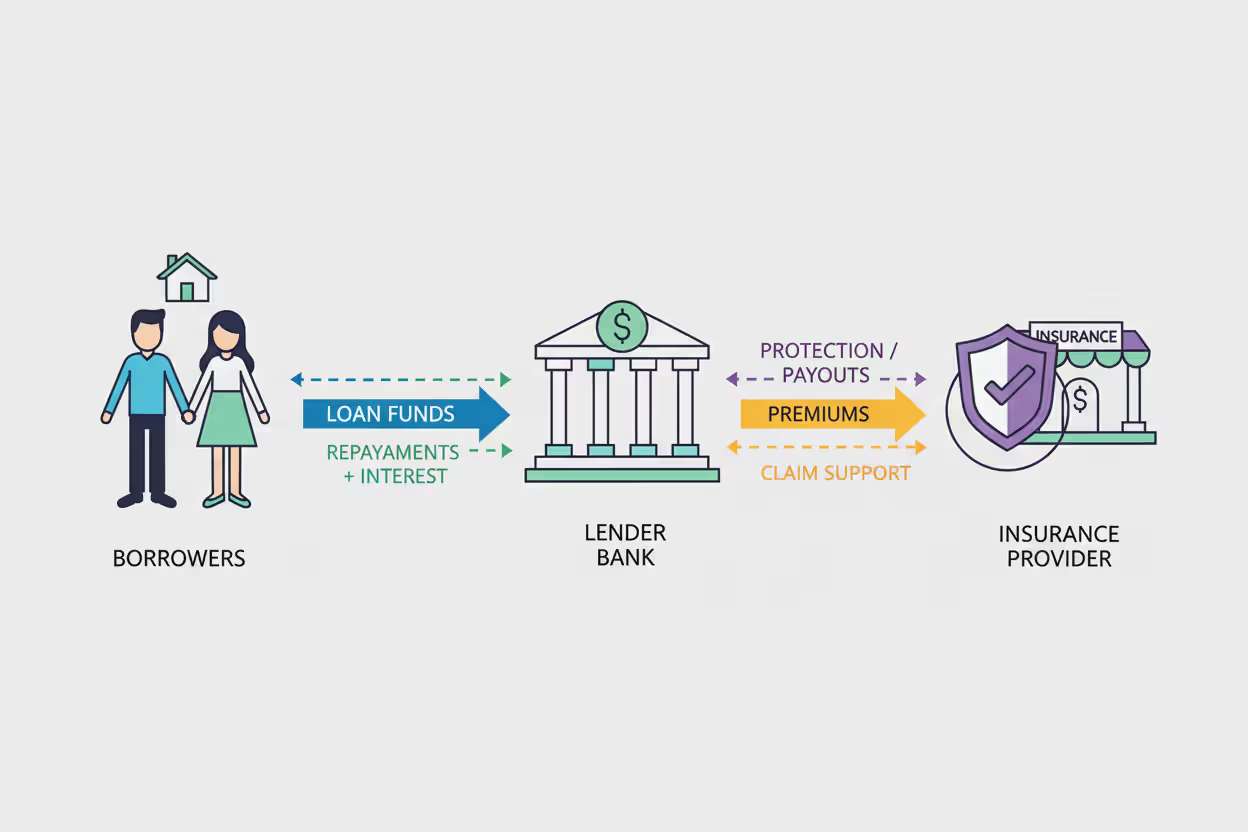

Think of PMI as a safety net—but not for you. Private mortgage insurance protects the bank or lender who approved your mortgage if you stop making payments and the home goes into foreclosure. You're footing the bill every month, but the coverage benefits the financial institution, not you as the homeowner.

Why does this system exist? Banks get nervous when borrowers put down less than 20% because there's less cushion if property values drop or if foreclosure becomes necessary. The mortgage insurance meaning here is simple: it shifts some of that default risk off the lender's books and onto an insurance company's balance sheet. This arrangement makes banks more comfortable approving loans for people who haven't accumulated a massive down payment yet.

Author: Brandon Kingswell;

Source: isomfence.com

Without this insurance option, most conventional lenders would flat-out refuse to work with anyone bringing less than 20% to closing. The private mortgage insurance explained in practical terms: it opened up homeownership to millions of Americans who have solid income and good credit but haven't spent a decade saving up 60 or 80 thousand dollars.

Most homebuyers first spot PMI when they're reviewing their Loan Estimate—that's the three-page standardized form your lender provides within three business days of your application. You'll see it listed as a separate monthly charge, sitting right there with your principal, interest, property taxes, and homeowners insurance. That line item shocks plenty of buyers who weren't expecting an extra $250 or $300 on top of everything else.

Here's what catches people off guard: you're paying to protect someone else's financial interest. If disaster strikes and you lose the house, the insurance company cuts a check to your lender to cover part of their loss. You still lose your home, your down payment, and take a massive hit to your credit score. The coverage doesn't help you one bit in that scenario.

When Lenders Require PMI

Banks require PMI on conventional mortgages whenever you're borrowing more than 80% of the home's value. They calculate this using your loan-to-value ratio, which is just your loan amount divided by the home's purchase price (or appraised value if that's lower).

Here's a real example: You're buying a $350,000 house and you've saved up $20,000 for your down payment. That's roughly 5.7%. You'll need to borrow $330,000, which gives you an LTV of 94.3% ($330,000 ÷ $350,000). Since you're above that 80% threshold, PMI becomes mandatory.

These pmi requirements apply specifically to conventional loans—the mortgages that aren't backed by government programs. Fannie Mae and Freddie Mac (the two massive quasi-government entities that buy most home loans from banks) set the rules here, and both of them insist on mortgage insurance when LTV crosses 80%.

One thing that surprises borrowers: having a 780 credit score won't exempt you from paying PMI if you're only putting 10% down. Your excellent credit will likely get you a lower PMI rate, which saves money. But you're still paying it. The 80% LTV cutoff applies across the board, regardless of how creditworthy you are.

Refinancing can trigger PMI requirements too, even if you'd been steadily paying down your original loan for years. Let's say you bought your home in 2020 with 20% down (no PMI), but now you want to refinance to get a better rate. If your home's value has dropped or you're taking cash out, your new loan might exceed 80% LTV—and boom, suddenly you're paying PMI on the refinance.

Some buyers assume PMI automatically drops off once they've paid their loan down to 80%. Not quite. There are specific rules about cancellation that we'll dig into, but it's not always automatic—sometimes you have to request it.

How Much Does PMI Cost

The pmi cost typically runs from 0.3% to 1.5% of your original loan amount per year. In dollar terms, that's roughly $75 to $375 monthly for every $100,000 you borrow.

Your specific premium depends on a handful of factors, and the range between best-case and worst-case scenarios is pretty dramatic:

Your credit score matters a lot. Borrowers with scores above 760 usually pay somewhere between 0.3% and 0.5% annually. Drop down to the 700-739 range and you're looking at 0.6% to 0.9%. Below 680? Rates can hit 1.2% or even higher. On a $280,000 loan, the difference between excellent credit and fair credit could mean paying an extra $1,200 per year.

Down payment size changes the equation. A 5% down payment carries much steeper premiums than 15% down. The insurance company views that 95% LTV as significantly riskier than 85% LTV, so they charge accordingly. Each additional percentage point you can put down typically reduces your PMI rate.

Loan size plays a role too. Bigger loans, especially those approaching the conforming loan limits (currently $806,500 in most areas for 2026), sometimes face slightly higher PMI rates. Insurance companies see more dollars at risk.

Here's something most people overlook: your debt-to-income ratio can nudge your PMI premium up or down. If you're already stretching to qualify with a 45% DTI ratio, some insurers will charge more than they would for someone at 30% DTI, even with the same credit score and down payment.

PMI Cost Comparison by Down Payment

| Down Payment | Loan Amount (on $300,000 home) | Estimated LTV | Annual PMI Rate | Monthly PMI Cost | Total First-Year Cost |

| 5% ($15,000) | $285,000 | 95% | 1.0% | $238 | $2,850 |

| 10% ($30,000) | $270,000 | 90% | 0.7% | $158 | $1,890 |

| 15% ($45,000) | $255,000 | 85% | 0.5% | $106 | $1,275 |

These estimates assume you've got credit scores in the 720-739 range. Your actual numbers will vary based on which mortgage insurance company your lender uses and your complete financial picture.

The cumulative impact becomes eye-opening when you project it over several years. With just 5% down, you might end up paying close to $10,000 in PMI premiums before you hit the equity threshold for cancellation. That's ten grand that doesn't reduce your loan balance or increase your ownership stake—it just evaporates.

How PMI Works Throughout Your Loan

Once you've closed on your home, how pmi works becomes pretty straightforward in terms of payment mechanics. Most buyers pay PMI monthly as part of their total mortgage payment. Your lender bundles it together with principal, interest, property taxes, and homeowners insurance into one amount that hits your bank account each month.

The lender collects your PMI premium and passes it along to the mortgage insurance company. This standard structure is called borrower-paid mortgage insurance (BPMI), though some alternatives exist that we'll cover in the next section.

Thanks to the Homeowners Protection Act that Congress passed back in 1998, you've got clear rights around PMI cancellation. Understanding these rules can prevent you from overpaying by months or even years.

Automatic termination kicks in at 78% LTV. Once your loan balance drops to 78% of your home's original appraised value, your lender must cancel PMI automatically—as long as you're current on payments. For a house originally valued at $300,000, this happens when you've paid your balance down to $234,000. You don't need to do anything; the lender handles it.

You can request cancellation at 80% LTV. Hit that 80% equity mark and you're allowed to ask your lender to remove PMI. Most lenders will require proof that your home's value hasn't declined, which usually means paying $400-600 for a new appraisal. They'll also typically want to see that you've made on-time payments for at least the past 12 months, with no 30-day late payments in the most recent six months.

Here's a scenario that trips people up all the time: Your home's value shoots up significantly because your neighborhood's gotten hot. Maybe you bought for $300,000 three years ago, and comparable homes are now selling for $375,000. Based on current market value, you might already have 20% equity even though your payment schedule wouldn't naturally get you there for another five years. You can potentially cancel PMI right now—but only if you take the initiative, order an appraisal, and formally request cancellation from your lender.

The law includes a midpoint safety valve too. If you haven't requested cancellation by the time you reach the halfway point of your loan term (15 years into a 30-year mortgage, for instance), the lender must automatically terminate PMI regardless of your current balance—assuming you're current on payments. This protects borrowers who aren't paying attention or don't realize they can act sooner.

Want to speed up the timeline? Making extra principal payments is one of the smartest moves. Let's say you've got a $285,000 loan at 6.5% interest. Adding just $200 extra to your principal every month could eliminate PMI roughly two years earlier than the standard amortization schedule, saving you several thousand dollars in premiums. The math definitely works in your favor if your budget can handle the additional payment.

Author: Brandon Kingswell;

Source: isomfence.com

Ways to Avoid or Remove PMI

You've got several paths to either skip PMI entirely or get rid of it faster than the standard timeline.

Author: Brandon Kingswell;

Source: isomfence.com

Save up 20% before you buy. This is the most obvious route—put down $60,000 on a $300,000 home and you'll never pay a dime of PMI. The downside? That might mean renting for an extra three to five years while you build up that cushion. Depending on your local market, home prices and rents might rise enough during that time to negate some or all of your PMI savings.

Lender-paid mortgage insurance flips the script. Some lenders offer to cover your PMI in exchange for charging you a higher interest rate—typically 0.25% to 0.5% more than you'd otherwise pay. The catch: you'll pay that higher interest rate for the entire loan unless you refinance, whereas PMI drops off once you hit 20% equity. This approach makes sense mainly if you're confident you'll refinance within three to five years, or if you really need to minimize your monthly payment in the short term.

Piggyback loans split your borrowing. This strategy, sometimes called an 80-10-10 loan, involves taking out two mortgages simultaneously: one covering 80% of the home's value (which avoids PMI since it's at exactly 80% LTV), a second smaller loan for 10%, and then you put down 10% in cash. The second mortgage is typically a home equity loan or HELOC with a higher interest rate. This approach lost popularity when interest rates climbed because that second loan got expensive fast.

Request early cancellation after appreciation. If your local real estate market's been booming, paying for a new appraisal might prove your home's increased value gives you 20% equity right now. Most lenders require you to have owned the home for at least two years (some want five years) before they'll consider cancellation based on appreciation rather than scheduled payment. But if your $280,000 purchase is now worth $340,000 after a few years, the $500 appraisal fee is absolutely worth it.

Refinance into a new mortgage. If your home has appreciated substantially—or if you've paid the loan down considerably—refinancing into a new loan at 80% LTV or better eliminates PMI from that point forward. You'll need to weigh refinancing costs (typically $2,000-5,000) and the new interest rate against your PMI savings. In today's rate environment, this works best if rates have dropped since you bought or if your home's value has jumped significantly.

Throw extra money at principal whenever possible. Even an extra $150 monthly can chop months off your PMI obligation. An annual bonus payment of a few thousand dollars accelerates things even more. Every dollar of extra principal gets you closer to that 80% LTV target.

I tell my clients that PMI shouldn't scare them away from buying if they're otherwise ready. Yes, it adds to your monthly cost. But it lets qualified buyers get into their own home now rather than renting for another three or four years while trying to save more. In markets where home values are climbing 5-7% annually, getting in now—even with PMI—usually builds wealth faster than staying on the sidelines

— Jennifer Martinez

PMI vs Other Types of Mortgage Insurance

Private mortgage insurance only exists on conventional mortgages. Government-backed programs have completely different insurance structures that work in their own ways.

FHA loans require MIP (mortgage insurance premium). You'll pay 1.75% of your loan amount upfront at closing, plus annual premiums between 0.55% and 1.05% depending on your loan term and how much you put down. The real kicker with FHA: if you put down less than 10%, that annual MIP stays in place for the entire 30 years. There's no cancellation option. You're stuck with it unless you refinance out of the FHA loan into a conventional mortgage. FHA loans allow down payments as low as 3.5%, which attracts a lot of first-time buyers—but that permanent insurance requirement costs you over the long haul.

VA loans charge a funding fee instead. Veterans Affairs mortgages don't have monthly mortgage insurance at all, which is fantastic. However, most borrowers pay a one-time funding fee at closing, usually ranging from 1.4% to 3.6% of the loan amount. The percentage depends on how much you're putting down (if anything) and whether this is your first VA loan or you've used the benefit before. Veterans with service-connected disabilities don't pay this fee. The big advantage: VA loans allow zero down payment for eligible service members and veterans.

USDA loans have guarantee fees. If you're buying in a qualified rural area, USDA loans require 1% upfront plus an ongoing annual fee of 0.35% of your remaining loan balance. Like FHA, this annual fee lasts for the loan's entire life. USDA loans also offer zero down payment options for eligible borrowers in approved areas.

The meaning of mortgage insurance across these programs stays consistent—protecting the lender (or the government program) when borrowers make small or zero down payments. PMI has one major advantage over FHA and USDA insurance: you can actually get rid of it once you've built up 20% equity. That makes conventional loans with PMI often smarter than FHA loans for borrowers who qualify for both, especially if they plan to stay in the home for more than five or six years.

Author: Brandon Kingswell;

Source: isomfence.com

Frequently Asked Questions About PMI

Private mortgage insurance will set you back somewhere between $75 and $375 monthly per $100,000 borrowed—that's real money adding up over time. Even though it only protects your lender, PMI serves a valuable function: it lets you buy a home years earlier than you could if you had to wait and save up a full 20% down payment.

The secret to managing PMI effectively? Stay on top of your loan balance and home value. Know your rights under federal law. Don't just wait around for automatic termination at 78% LTV—if you hit 80% equity (either through payments or appreciation), speak up and request cancellation. Think about strategies like accelerated principal payments, which can eliminate PMI years earlier and potentially save you $5,000 to $10,000 in total premiums.

Remember this crucial distinction: PMI is temporary, unlike FHA mortgage insurance that typically sticks around for 30 years. For buyers who can qualify for conventional financing, accepting PMI for a few years usually beats choosing an FHA loan or postponing homeownership indefinitely while trying to save more. Crunch the numbers for your particular situation, factor in what's happening with home values in your market, and make the decision that aligns with where you want to be financially in five or ten years.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to home loans, mortgage rates, home equity loans, and the home buying process.

All information, including articles, guides, and explanations, is provided for general educational purposes only. Mortgage terms, interest rates, eligibility requirements, and lending conditions may vary depending on individual financial situations, lenders, and regional regulations.

This website does not provide financial, legal, or mortgage advice, and the information presented should not be considered a substitute for consultation with qualified financial professionals, lenders, or advisors.

The website and its authors are not responsible for any errors or omissions, or for any decisions made based on the information provided on this website.