Homeowner comparing HELOC and home equity loan options at a table

HELOC vs Home Equity Loan Guide

You've built up serious equity in your home—maybe $150,000, maybe more. Now you're wondering: should I tap into it through a credit line I can use whenever, or just take out one big loan all at once?

Here's the thing: these aren't interchangeable products with slightly different labels. They work completely differently, cost different amounts, and one will probably match your situation way better than the other.

Getting this choice wrong? You could end up with payments that double overnight, or locked into a loan charging interest on money just sitting in your checking account. Let's figure out which one actually makes sense for you.

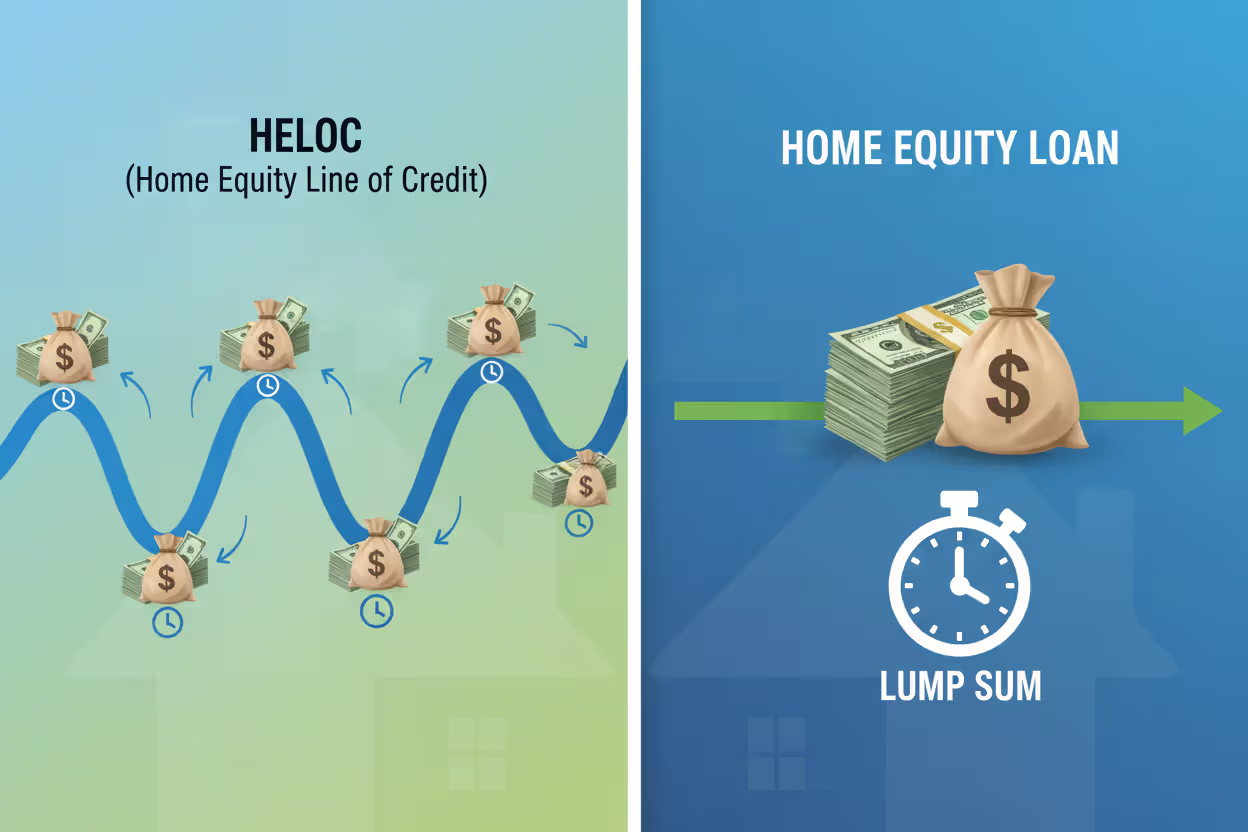

What Are HELOCs and Home Equity Loans?

Both let you borrow against the ownership stake you've built in your property. Let's say your place appraises at $400,000 and your remaining mortgage is $200,000—you've got $200,000 in equity sitting there. Banks will typically front you somewhere between 80-90% of that equity, after subtracting what you still owe.

Here's where things split: one product hands you a pile of cash upfront, the other gives you a credit line you can tap into over time. That fundamental difference between HELOC and home equity loan structures? It'll determine everything from what you pay monthly to whether your rate can suddenly jump.

Author: Brandon Kingswell;

Source: isomfence.com

Home Equity Line of Credit Explained

Think of this like getting a credit card that's backed by your house. The bank approves you for, say, a $100,000 limit. Then for the next decade (usually), you can pull money out whenever you need it.

Maybe you take $15,000 in year one for that kitchen backsplash. Year three, the HVAC dies and you grab another $8,000. The rest just sits there, available if you need it but not costing you anything.

During this borrowing window (they call it the "draw period"), most lenders only make you pay interest on whatever you've actually used. Sounds great, right? Here's the catch: once that 10-year window closes, you can't borrow anymore AND your payments usually spike—now you're paying back everything you borrowed plus interest, typically over the next 10-20 years.

Most HELOCs don't have fixed rates. They're tied to something called the prime rate, which moves when the Federal Reserve fiddles with interest rates. Your neighbor might've watched her monthly payment swing from $340 to $625 last year just from rate changes. Some lenders cap how high your rate can climb, but you're still riding a roller coaster compared to fixed-rate options.

Home Equity Loan Explained

This one's straightforward: you borrow a specific amount, they deposit it all at once, and you start paying it back immediately. Need $50,000? You get $50,000 wired to your account, usually within a few weeks.

Your rate gets locked in on day one. If you close at 7.5% this month, you're paying 7.5% until the loan's paid off—whether that's five years or twenty. The Fed could slash rates in half next year, and you're still at 7.5%. They could double them, and you're still at 7.5%.

That predictability comes with a downside, though: you're paying interest on every dollar from the start. Borrowed $50,000 but only needed $35,000 right away? Too bad—you're paying interest on that extra fifteen grand while it earns basically nothing in your savings account.

Key Differences Between HELOC and Home Equity Loan

When you compare a home equity line of credit with a loan, you'll spot several deal-breakers depending on your situation:

How you get the money: HELOCs work like a spigot you can turn on whenever for about a decade. Home equity loans? One deposit, that's it.

Rate stability: HELOCs have rates that bounce around with the market. During 2025-2026, people saw their monthly bills swing $200-400 as the Fed kept adjusting rates. Fixed-rate home equity loans never budge.

What you pay monthly: HELOCs often let you pay just interest for the first chunk of years—feels cheap until suddenly you're paying back principal too and your payment potentially triples. Home equity loans hit you with the same payment every single month from start to finish.

Getting more money later: Two years in, need another $10,000 with your HELOC? Just draw it (assuming you haven't maxed out). With a home equity loan? You're applying for a whole new loan.

The loan versus line of credit for home equity decision really comes down to this: do you need payment consistency or borrowing flexibility more?

| Feature | HELOC | Home Equity Loan |

| How You Get Money | Pull out what you need, when you need it, up to your limit | One lump sum deposited at closing |

| Rate Type | Adjustable (moves with prime rate) | Locked in for the entire repayment period |

| Monthly Payments | Often interest-only at first, then principal + interest kicks in | Same payment of principal + interest from day one |

| Borrowing Window | Usually 10 years to draw funds | No draw period—one-time funding only |

| Total Timeline | 20-30 years combined (draw period + repayment) | 5-20 year terms most common |

| Works Best For | Projects with changing costs, ongoing needs, financial cushion | Single large expense, consolidating debt, predictable budgets |

| Upfront Fees | Often $0-500 (sometimes waived entirely) | Typically $500-3,000 |

When to Choose a HELOC Over a Home Equity Loan

HELOCs shine when you can't nail down exact costs or timing. Here's when they make sense:

You're renovating in phases: Ever seen a remodel go exactly as planned? Neither have contractors. You might demo the bathroom in month one, but discover the subfloor's rotted and now you need an extra $6,000. Then the tile you wanted gets backordered three months. A HELOC lets you pay for stuff as it actually happens—you're not paying interest on bathroom tile money while waiting for the plumber to finish.

Your income jumps around: Freelance graphic designer? Sales rep working on commission? Real estate agent? Some months you're flush, others you're sweating the mortgage payment. A HELOC gives you a safety net for lean periods without forcing you to pay interest on money you haven't touched.

College bills are coming: Tuition doesn't hit all at once—it's semester by semester for four years. Why borrow $120,000 upfront when you can pull out $30,000 each year? Especially if your kid might snag a scholarship junior year or transfer somewhere cheaper.

You're tackling credit card debt strategically: Got $35,000 across five cards you're systematically paying down? A HELOC lets you transfer balances as you knock them out, rather than borrowing the full amount when you might not need it all.

The heloc or home equity loan question often boils down to: can you predict your exact costs and timing? If not, the HELOC's flexibility beats its rate risk.

Real example: A couple in Portland got a $75,000 HELOC for a kitchen renovation budgeted at $50,000. Contractor opened up the wall and found knob-and-tube wiring—another $18,000 to bring everything up to code. They just drew the extra funds. A fixed home equity loan would've left them scrambling to find another lender mid-project.

Author: Brandon Kingswell;

Source: isomfence.com

When a Home Equity Loan Makes More Sense

Sometimes you need the structure and predictability that only a lump sum loan delivers:

You're consolidating debt with a plan: You've got $40,000 spread across credit cards at 22% APR. Consolidating into a 7.8% home equity loan saves a fortune—plus that fixed payment creates discipline. You can't just make minimums forever when there's a set payoff date.

Big one-time purchase: Buying a rental property? Making a down payment on your kid's business? Paying for a wedding? You know exactly what it costs. Borrow that amount, lock your rate, and follow a clear payoff timeline.

Rates are low or climbing: When mortgage rates are unusually cheap or everyone's predicting increases, locking in a fixed rate protects you. People who grabbed 5.5% home equity loans in early 2024? They're thrilled they're not paying the 7-8% rates everyone's getting now in 2026.

Credit lines tempt you to overspend: Be honest with yourself—would having $75,000 sitting there available make you rationalize purchases you don't really need? A one-time loan removes that temptation completely.

You're paying this off fast: Planning to throw extra payments at it and be done in three years? The fixed structure keeps you accountable. HELOCs' interest-only periods can make it too easy to procrastinate on actually paying down the balance.

A couple in Phoenix used a $60,000 home equity loan for solar panels and a new HVAC—both projects had fixed bids and wrapped up in six weeks. Their $587 monthly payment never changed, and they knew they'd be debt-free in exactly ten years.

Author: Brandon Kingswell;

Source: isomfence.com

Costs and Requirements Comparison

You'll need similar qualifications for either, but the fee structures and approval process differ a bit.

Credit requirements: Most lenders want at least 620-680 for either option. Want the best rates (under 8% these days)? You'll need 700 or higher. HELOCs sometimes require slightly better credit since the variable rate adds risk for the lender.

Equity requirements: Banks usually cap your combined mortgage and home equity debt at 80-90% of your home's value. Own a $400,000 house with $200,000 left on the mortgage? You could potentially access $120,000-160,000 depending on the specific lender's rules.

Proving your income: Both require pay stubs, tax returns, and they'll check your debt-to-income ratio—usually wants to see that under 43%. Self-employed? Get ready for extra paperwork either way.

What you'll pay upfront: Home equity loans typically run $500-3,000 in closing fees—appraisal, title search, origination charges, the works. HELOC lenders? Many waive fees entirely to compete for your business, though some charge $50-100 annual maintenance fees.

Appraisal costs: Both usually require a professional appraisal running $400-600. Some lenders skip it for smaller amounts or if you've got excellent credit and tons of equity.

Timeline to funding: Home equity loans usually take 2-4 weeks to close. HELOCs often move faster—sometimes 10-14 days—partly because lenders can freeze your credit line if they get nervous about your property value dropping.

Here's the thing about the heloc versus home equity loan cost comparison: a no-fee HELOC looks amazing initially. But if rates climb 2-3 percentage points over five years, you might end up paying more total interest than if you'd just paid the upfront fees and locked in a fixed rate.

Common Mistakes When Choosing Between the Two

Author: Brandon Kingswell;

Source: isomfence.com

Forgetting about payment shock: People focus on that sweet $200 interest-only HELOC payment during the draw period. Then year eleven hits and suddenly it's $550 because now they're paying principal back too. Plan for the real payment, not the teaser payment.

Borrowing up to your max: Just because they approved you for $100,000 doesn't mean you should take it. Borrow what you actually need plus maybe 10-15% cushion for surprises. Over-borrowing puts your house at risk if you lose your job or face unexpected expenses.

Not checking how often rates adjust: Some HELOCs adjust monthly, others quarterly or annually. Monthly adjustments mean more payment volatility. And read about the caps—how much can the rate jump per adjustment, and what's the maximum over the life of the loan?

Assuming the interest is tax deductible: Quick heads up: under current tax law, you can only deduct home equity interest if you used the money to improve the property securing the loan. Using it to pay off credit cards or start a business? Generally not deductible. Check with your tax person, don't just assume.

Chasing the lowest advertised rate: That HELOC at 6.5% looks way better than the home equity loan at 7.8%. Until the HELOC rate adjusts to 9.5% eighteen months from now. Run the numbers on what you'd actually pay if rates climb a couple points.

Ignoring prepayment penalties: Some home equity loans charge fees if you pay them off early. Planning to sell your house or refinance in three years? Make sure the loan doesn't penalize you for that.

The biggest mistake I see is homeowners choosing a HELOC for its lower initial payment without modeling what happens when rates rise or the draw period ends. If you can't comfortably afford the fully-amortized payment at a rate 2-3 points higher than today's, you're taking on too much risk. For most single-purpose borrowing needs, the predictability of a fixed-rate home equity loan provides better long-term financial stability

— Jennifer Martinez

Frequently Asked Questions

The heloc or home equity loan decision isn't about finding the objectively superior product—it's about matching the right tool to your specific situation, timeline, and how much uncertainty you can stomach.

Go with a HELOC when you need ongoing access to money, you're okay with payments that might fluctuate, and you only want to pay interest on what you actually use. This works for multi-phase projects, emergency funds, and situations where you honestly can't predict the total cost upfront.

Pick a home equity loan when you need a specific lump sum, you value knowing exactly what you'll pay monthly, and you want today's rate locked in. This structure fits one-time expenses, debt consolidation with a clear payoff plan, and borrowers who prefer structured repayment they can't wiggle out of.

Before signing anything, run some worst-case scenarios: What if rates jump 2%? What if you lose 20% of your income? What if you need to sell in three years? The right choice gives you the financial flexibility you need without putting your home at unnecessary risk.

Both products can be smart ways to use your home's value—but only when you choose strategically and borrow responsibly. Compare actual offers from multiple lenders, read the fine print on rate adjustment terms and fees, and consider talking to a financial advisor if your situation involves complicated tax implications or you're borrowing a significant chunk of your equity.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to home loans, mortgage rates, home equity loans, and the home buying process.

All information, including articles, guides, and explanations, is provided for general educational purposes only. Mortgage terms, interest rates, eligibility requirements, and lending conditions may vary depending on individual financial situations, lenders, and regional regulations.

This website does not provide financial, legal, or mortgage advice, and the information presented should not be considered a substitute for consultation with qualified financial professionals, lenders, or advisors.

The website and its authors are not responsible for any errors or omissions, or for any decisions made based on the information provided on this website.