Homeowner reviewing home equity loan documents at a table

Home Equity Loan Requirements Guide

Thinking about borrowing against your house? The approval gauntlet you'll face makes applying for your first mortgage look like filling out a library card application. Banks don't care that you've paid on time for eight years—they're going to pick apart your finances like an auditor investigating fraud.

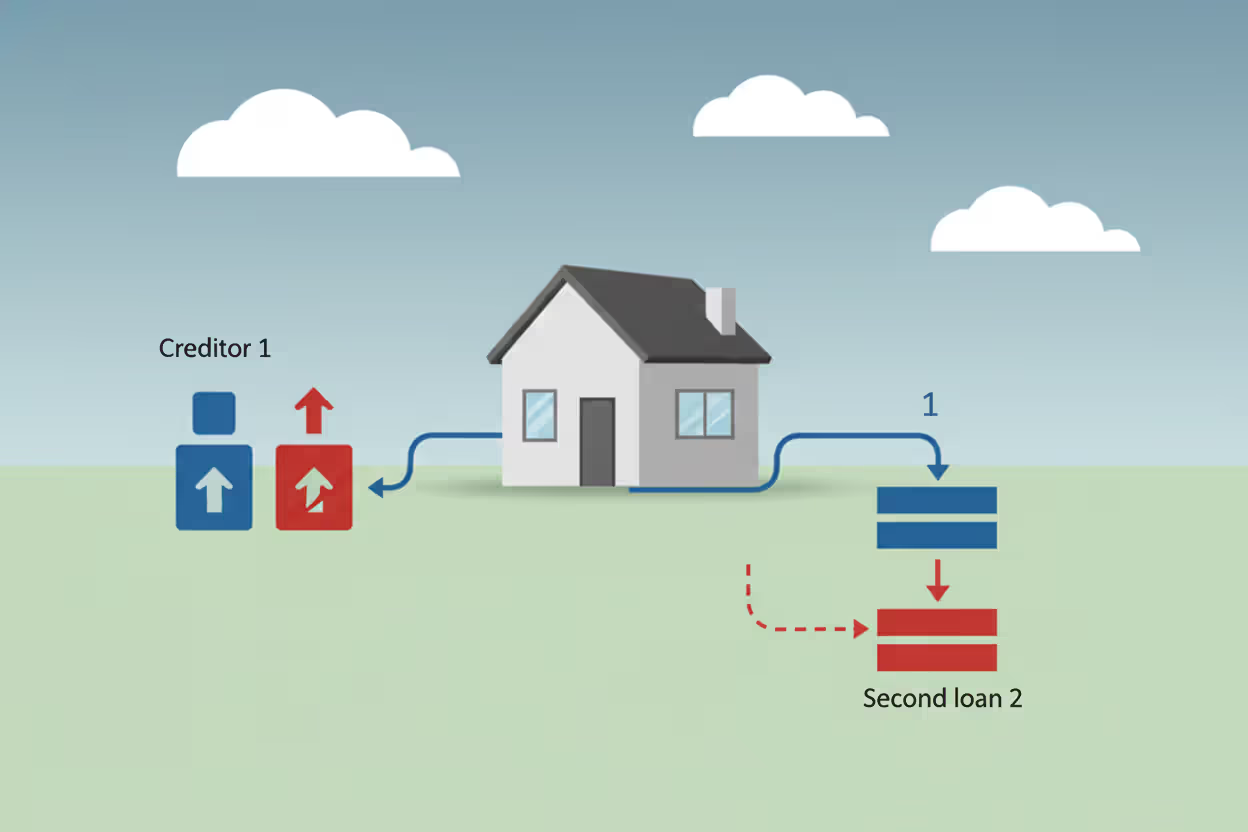

Here's how these loans work: You get a lump sum deposited into your account, then repay it through identical monthly installments over whatever term you've agreed to (usually 10-20 years). Your existing mortgage keeps chugging along unchanged. This new debt tags along behind it in what lenders call "subordinate lien position."

That technical term matters more than you'd think. Picture a foreclosure scenario where the bank auctions your property. The original mortgage holder collects their money first from whatever the house sells for. Only then—if anything remains—does your home equity lender get paid. Since they might collect nothing in a worst-case scenario, they protect themselves by making qualification harder than scaling a cliff without ropes. You'll need pristine credit, massive accumulated equity, rock-solid income proof, and minimal existing bills. Fall short anywhere? You're either getting rejected outright or stuck with an interest rate so ugly you'll wish you'd never applied.

What Are Home Equity Loan Requirements?

Author: Ethan Callahan;

Source: isomfence.com

Banks evaluate five core components when reviewing applications: payment track record and credit standing, accumulated ownership stake in the property, documented income sources, current monthly obligations, and the physical home itself. Individual banks set different cutoffs, but these five categories remain universal.

Why such aggressive vetting? The Dodd-Frank reforms that followed the 2008 housing crash legally require lenders to verify actual repayment capacity before approving loans. They can't greenlight applications based purely on property worth anymore—that approach destroyed the economy fifteen years ago. Today they must prove you genuinely have the financial means to repay.

Typical loan sizes range from $10,000 up to $500,000, spread across terms between 5 and 30 years. That's serious money you're committing to repay. Banks need confidence your financial situation will hold steady throughout that entire stretch, not just look good on today's application.

Some lenders apply what they call "compensating factors"—crushing it in one qualification area can offset mediocre performance elsewhere. Someone sporting an 820 credit score might squeak through despite debt levels that would sink a 690-score applicant. Credit unions and portfolio lenders (who keep loans on their own books instead of selling them to investors) tend toward this flexibility more than big national banks.

Minimum Credit Score and Credit History Standards

The baseline sits around 620 for most mainstream lenders, though qualifying at that floor typically means swallowing rates 2-3 points higher than borrowers with excellent credit pay. Not exactly a bargain.

Big banks generally want 680-700 before they'll offer anything resembling competitive pricing. Credit unions sometimes accept members down to 640, especially folks who've banked with them for years. Online lenders scatter across the entire spectrum—some chase subprime borrowers starting at 580, while others slam the door on anyone below 720.

Your three-digit number matters less than you'd guess. What happened during the previous 12-24 months carries substantially more weight. One payment landing 30 days late within the past year can destroy your application or force you into punishing terms. Several recent missed payments? Don't waste your time applying.

Bankruptcy creates mandatory waiting periods before you can qualify. Chapter 7 discharges typically require waiting 4 years, though some lenders shorten this to 2 years when you prove extenuating circumstances (catastrophic medical crisis, divorce, sudden unemployment) and show you've rebuilt credit since filing. Chapter 13 occasionally allows approval after 2 years if you've maintained perfect payment records through your trustee. Foreclosure? Plan on sitting out 7 years at most institutions.

Short sales and deeds-in-lieu fall somewhere in between—expect 4-5 year holding patterns. Portfolio lenders occasionally bend these timelines for borrowers with massive equity cushions and bulletproof income, but I wouldn't count on finding one.

One bright spot: shopping around won't trash your score if you compress all applications into a 14-45 day window. Credit bureaus recognize legitimate comparison shopping versus racking up new debt, so they treat those inquiries as a single event. Still, I'd limit yourself to 4-5 lenders maximum to avoid unnecessary dings.

Equity and Loan-to-Value Ratio Requirements

Banks demand you keep at least 15-20% equity after they cut you the check. Translated into banking jargon, that means 80-85% combined loan-to-value (CLTV) maximums.

Let's run actual numbers. Your house appraises for $400,000 and you still owe $280,000 on the original loan. You've built up $120,000 in equity (30% of the home's value). If your lender sets an 80% CLTV limit, all mortgages combined can't exceed $320,000. Subtract your existing $280,000 balance, and you can borrow up to $40,000.

Author: Ethan Callahan;

Source: isomfence.com

Here's where people get blindsided: the appraiser your lender hires determines what your property's worth, end of discussion. Your county tax assessment? Totally meaningless. That Zillow estimate? Might as well be Monopoly money. When you're absolutely certain your place is worth $450,000 but it appraises at $400,000, you just lost $50,000 in borrowing power.

CLTV limits shift based on your credit profile. Borrowers above 740 might access 85-90% at certain banks. Those between 680-739 typically max out around 80-85%. Below 680? Figure on 75-80% caps, if you get approved at all.

Watch for minimum loan amounts, usually $10,000-$25,000. This creates an infuriating trap for borrowers without much equity. Say your property's worth $200,000 with $150,000 still owed. That's $50,000 in accumulated equity. At 80% CLTV, you hit a $160,000 maximum combined total. Subtract your $150,000 mortgage and you can borrow $10,000. When the bank requires $15,000 minimum, you're stuck—not enough equity to meet the threshold, too much debt to make a full refinance worthwhile.

Maximum loan amounts usually cap at $250,000-$500,000 regardless of how much equity you've accumulated. Jumbo home equity products exist above these ceilings but require immaculate qualifications—think 760+ scores and exhaustive income documentation.

Investment properties face tighter restrictions. Figure on 70-75% maximum CLTV, meaning you must keep 25-30% equity. Vacation homes land between primary residences and pure rentals, generally requiring 20-25% equity retention.

Income and Debt-to-Income Ratio Criteria

W-2 employees enjoy the simplest documentation process: recent pay stubs covering the last 30 days, W-2 forms from the past two years, plus permission to contact your employer directly. Most lenders call your HR department within days of closing to verify you're still employed—borrowers occasionally lose their jobs right before closing and try hiding it.

Self-employed applicants? Buckle up for serious paperwork demands. You'll provide two full years of personal tax returns including every single schedule, current year profit and loss statements, and often business bank statements on top of that. Lenders calculate average income across 24 months, which penalizes recent business growth. Made $60,000 two years back and $100,000 last year? They'll use $80,000 for qualification purposes despite your earnings climbing.

Author: Ethan Callahan;

Source: isomfence.com

The debt-to-income ratio compares your monthly debt payments against gross monthly earnings. Most lenders draw the line at 43%, though some stretch to 50% with compensating factors like exceptional credit or substantial cash reserves.

What counts as debt? Your first mortgage payment, the proposed home equity loan payment, car loans, student loans, minimum credit card payments, personal loans, and any installment debts. What doesn't count? Utility bills, insurance premiums (unless part of your mortgage escrow), groceries, gas, and other daily living costs.

Let's examine a real-world example. Monthly gross income totals $8,000. Current debts include $1,800 for your mortgage, $400 for a car loan, $250 for student loans, and $150 in credit card minimums. That's $2,600 monthly. The home equity loan adds $500 per month. Total debt hits $3,100, producing a 38.75% ratio ($3,100 divided by $8,000).

Non-employment income faces heavy scrutiny. Rental income? They'll count 75% of gross rents to account for vacancies and upkeep. Social Security and pension payments count at 100% if guaranteed to continue at least three more years. Alimony and child support qualify when you document 12 months of consistent receipt with at least three years remaining.

Commission and bonus pay requires two-year track records. Lenders average this income and may ignore it entirely when trending downward. A sales rep earning $40,000 base plus $30,000 in commissions two years ago but only $15,000 in commissions last year might see commission income averaged to $22,500 or potentially excluded completely.

Property and Appraisal Requirements

Single-family primary residences get the warmest reception. Condos and townhouses qualify but trigger extra scrutiny—the entire condo project must meet lender standards. They typically want at least 50% owner-occupancy, fewer than 15% of units behind on HOA dues, and no active lawsuits involving the association.

Two-to-four-unit buildings qualify when you live in one unit yourself. Expect lower maximum CLTV ratios, typically capped at 75-80%. Pure rental properties qualify through some lenders, but requirements get considerably tougher.

Manufactured housing gets messy. Units built after June 15, 1976 (meeting HUD construction standards) and permanently anchored to land you own might qualify. Older mobile homes or those sitting in parks where you rent the pad? Traditional approval proves extremely difficult.

Rural properties with extensive land face restrictions. Most residential lending programs cap eligible property at 10-20 acres. Farms and ranches exceeding this get pushed into specialized agricultural financing.

Appraisals run $400-$600 and need 1-2 weeks to complete. You can't use an appraisal you paid for yourself—lenders order them from their approved vendor lists. The appraiser examines inside and outside, compares against recently sold similar properties nearby, and adjusts for differences in size, upgrades, and condition.

Author: Ethan Callahan;

Source: isomfence.com

Property condition matters enormously. Significant deferred maintenance, structural problems, or safety issues can trigger repair requirements or complete denial. Peeling paint outside, damaged roof, broken heating system, or foundation cracks frequently need addressing before closing. Some lenders create repair escrows holding loan money until you complete the work, though this adds weeks and complications.

Occupancy status dramatically affects approval chances. You'll sign documents swearing you plan to live in the property as your primary home—most lenders define this as spending at least 6 months yearly there. Second homes require proving you own another primary residence and aren't renting the property out. Rental properties must be disclosed accurately—lying about occupancy status constitutes mortgage fraud with potential criminal charges.

Required Documentation for Home Equity Loan Approval

Get organized before submitting applications, not after. Missing paperwork causes most timeline delays. Build your document file first, then start shopping lenders.

Financial Documents

Recent pay stubs from the last 30 days show current income and year-to-date totals. Weekly pay schedule? Provide 4-5 stubs. Bi-weekly needs 2-3. Monthly requires just the latest one.

Last two years of W-2 forms establish income consistency. Self-employed people substitute complete tax returns—Form 1040 plus every schedule, especially Schedule C for sole proprietors, Schedule E for rental properties, or K-1s for partnership income.

Bank statements covering the previous 60 days for all accounts prove assets for closing costs and reserves. Lenders examine large deposits closely. Anything exceeding $500-$1,000 needs explanation. Payroll deposits, transfers between your own accounts, or documented family gifts pass inspection. Unexplained cash deposits raise concerns about unreported income or borrowed money.

Investment and retirement account statements show additional assets. You probably won't drain your 401(k) for closing costs, but substantial reserves strengthen borderline applications.

Current credit card and loan statements help lenders calculate accurate ratios. Don't try hiding obligations—they'll appear on your credit report anyway, and omissions signal dishonesty.

Property Documents

Your current mortgage statement shows the remaining balance, monthly payment, and account status. Lenders verify payoff amounts directly with your servicer, but your statement provides a starting reference.

Homeowners insurance declaration page proves adequate coverage. Most lenders want coverage matching either the loan amount or replacement value, whichever is lower.

Property tax bills from the past year confirm you're current. Delinquent property taxes derail approvals immediately since tax liens supersede mortgages during foreclosure.

HOA documentation (for condos and planned communities) includes recent statements showing current status, CC&Rs (rules and restrictions), and the association's master insurance policy.

Your deed confirms ownership. Most lenders obtain this through their title company, but having a copy ready speeds things along.

Identity Verification

Government-issued photo ID (driver's license or passport) verifies your identity. The name on your ID must match your loan application exactly—even minor variations like "Bob" versus "Robert" create delays.

Social Security card or other SSN documentation enables credit report pulls and IRS income verification when needed.

Proof of address matters mainly for investment property loans where you're not living in the home. Utility bills or lease agreements for your actual residence work fine.

Timeline expectations: budget 30-45 days from application submission to closing. Well-prepared applications with responsive appraisers occasionally close in 20-25 days. Complications like property problems, income verification challenges, or title snags can stretch the process past 60 days.

Common Reasons for Home Equity Loan Denial

Credit problems lead rejection statistics by a wide margin. Scores falling below minimums trigger automatic denials. Recent late payments, maxed-out credit cards (utilization exceeding 30-40%), or numerous recent credit inquiries damage applications significantly. Collections and charge-offs—even tiny balances—often cause denial unless you pay or settle them before submitting applications.

Author: Ethan Callahan;

Source: isomfence.com

Fix credit problems before applying rather than crossing your fingers that lenders will overlook them. Get your credit reports from all three bureaus (Experian, Equifax, TransUnion) at AnnualCreditReport.com. Spot errors? Start disputes immediately—resolution takes 30-45 days. Pay credit card balances down under 30% of your limits. Hold off on opening new credit accounts for six months before applying.

Insufficient equity affects many applicants, especially recent buyers or those in markets experiencing price declines. Bought with 10% down two years ago and prices dropped 5%? You might have minimal equity left. Your only solutions involve paying down your original mortgage or waiting for prices to recover—neither happens quickly.

Excessive debt ratios cause denials when monthly obligations eat up too much income. You've got two options: boost income (rarely realistic on short notice) or reduce debt. Eliminate smaller debts completely rather than spreading payments across multiple accounts. That $5,000 car loan costing $200 monthly? Pay it off entirely and remove the full payment from calculations. Paying $2,500 toward a $10,000 loan might only reduce monthly payment by $100.

Property problems range from cosmetic to catastrophic. Minor cosmetic issues rarely matter, but structural concerns, safety hazards, or failed systems require resolution. An appraiser flagging a damaged roof might require replacement or repair before closing. Budget for potential property fixes when planning your application—assuming your home will cruise through appraisal clean often proves overly optimistic.

Employment instability raises red flags. Frequent job hopping, recent career switches to entirely new industries, or transitions from W-2 employment to self-employment all create concerns about income continuity. Changed jobs recently? Wait until you've cleared any probationary period and received at least one paycheck before applying. Self-employed borrowers should wait at least two years after starting their business—most lenders require that income history minimum.

Title complications occasionally emerge during applications. Unpaid contractor liens, divorce decree complications, or inheritance disputes can cloud title. These require resolution before any lender proceeds. Work with a real estate attorney if title problems surface—they rarely resolve easily or quickly.

Appraisal shortfalls frustrate borrowers convinced their homes exceed the appraised value. You can challenge appraisals by providing comparable sales the appraiser overlooked, but success rates run low. Most appraisers thoroughly research comparable sales and won't revise values without compelling new evidence. When your appraisal comes in low, you can reduce your loan request, bring cash to closing to compensate for the equity gap, or abandon the application.

The appraisal surprises more borrowers than any other part of qualifying for home equity loans.People obsess over credit scores and income documentation but assume their home will appraise at whatever value they've imagined. I've watched countless applications stall or collapse because appraisals came in 5-10% below expectations. In hot markets, tax assessments lag behind actual values, giving borrowers false confidence. In declining markets, they're shocked when recent comparable sales show lower values than what they paid. My advice? Always budget conservatively and assume your home might appraise 5% below your estimate—that cushion prevents disappointment and preserves your borrowing flexibility

— Jennifer Martinez

Frequently Asked Questions

Getting approved for a home equity loan demands preparation across multiple financial dimensions. Your credit profile, equity position, income stability, and property condition all carry equal weight—exceptional strength in one area rarely compensates for serious weakness in another.

Begin by checking your credit reports and fixing problems well before applying. Calculate available equity conservatively, assuming your home might appraise below your estimate. Organize financial documentation systematically, gathering pay stubs, tax returns, bank statements, and property documents before starting applications.

Shop multiple lenders rather than accepting the first offer. Credit unions, traditional banks, and online lenders impose different standards and offer varying rates. A 680 credit score might get rejected at one institution but approved at competitive rates elsewhere.

Remember that requirements protect you as much as the lender. Banks need confidence you'll repay the loan over 10-30 years. Meeting these standards protects you from overextending financially just as much as it safeguards the lender's investment.

When you don't qualify today, use specific denial reasons to build an improvement plan. Most credit issues resolve within 6-12 months with focused effort. Equity accumulates through principal payments and appreciation over time. Income stability improves as you establish longer employment history.

Home equity loans provide valuable access to your property's value for debt consolidation, home improvements, education expenses, or other significant needs. Meeting the requirements opens that door—rushing in unprepared guarantees rejection and wasted time.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to home loans, mortgage rates, home equity loans, and the home buying process.

All information, including articles, guides, and explanations, is provided for general educational purposes only. Mortgage terms, interest rates, eligibility requirements, and lending conditions may vary depending on individual financial situations, lenders, and regional regulations.

This website does not provide financial, legal, or mortgage advice, and the information presented should not be considered a substitute for consultation with qualified financial professionals, lenders, or advisors.

The website and its authors are not responsible for any errors or omissions, or for any decisions made based on the information provided on this website.