Homeowner reviewing home equity loan documents at a table

Home Equity Loan Rates Guide

Content

Content

Borrowing against your home's equity can unlock tens of thousands of dollars for renovations, debt consolidation, or major expenses. Unlike credit cards or personal loans, home equity loans offer substantially lower borrowing costs because your property secures the debt. Understanding how lenders price these loans—and what drives the rates you'll actually pay—makes the difference between a smart financial move and an expensive mistake.

What Are Home Equity Loan Rates and How Do They Work

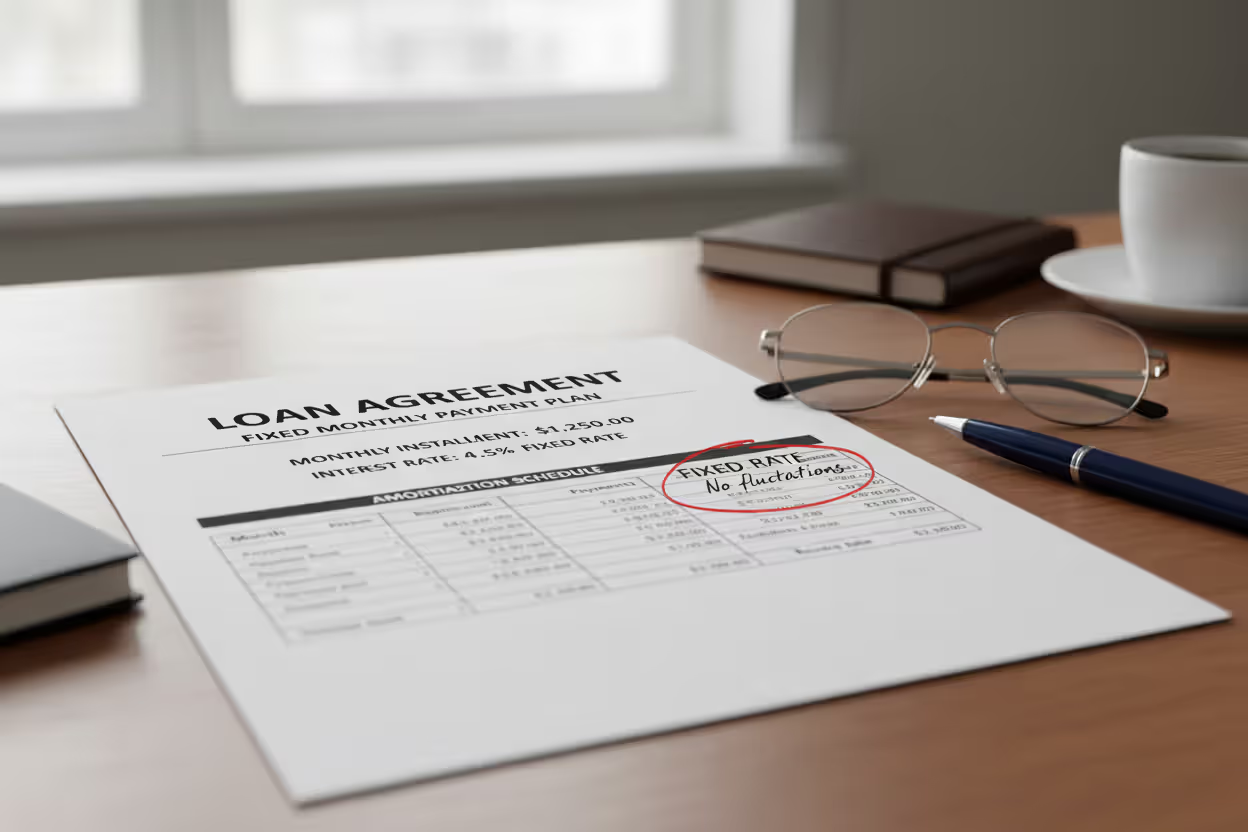

A home equity loan rate represents the annual cost of borrowing against the portion of your home you own outright. When you take out a home equity loan, the lender provides a lump sum that you repay over a fixed term, typically 5 to 30 years, with monthly payments that include both principal and interest.

Most home equity loans carry fixed rates, meaning your interest percentage stays constant throughout the entire repayment period. This differs sharply from home equity lines of credit (HELOCs), which usually feature variable rates tied to the prime rate or another benchmark index. A HELOC works like a credit card secured by your home—you draw funds as needed up to a credit limit—while a home equity loan delivers all the money upfront in one disbursement.

The rate structure on a home equity loan is straightforward: the lender quotes an annual percentage rate (APR) that reflects both the interest rate and certain fees. Your monthly payment remains identical from the first month to the last, which simplifies budgeting. If you borrow $50,000 at 7.5% over 15 years, you'll pay approximately $463 per month regardless of what happens to broader interest rates during that period.

Author: Hannah Whitlock;

Source: isomfence.com

Some lenders offer variable-rate home equity loans, though these remain less common. With a variable product, your rate adjusts periodically based on an underlying index plus a margin. Your payment can rise or fall, introducing uncertainty but sometimes starting with a lower initial rate than fixed alternatives.

Average Home Equity Loan Rates in 2026

Home equity loan rates currently range from approximately 6.75% to 11.50%, depending primarily on your creditworthiness and the lender you choose. Borrowers with excellent credit and substantial equity typically secure rates in the 6.75% to 8.25% range, while those with fair credit or higher loan-to-value ratios may face rates above 9.5%.

These rates reflect the Federal Reserve's monetary policy stance heading into 2026. After aggressive rate increases in 2022 and 2023, the Fed made modest cuts in 2024 and 2025, bringing the federal funds rate to a range that supports moderate borrowing costs. Home equity loan rates generally track 1 to 3 percentage points above the prime rate, which stands at approximately 6.50% in early 2026.

Historical context matters: before the 2022 rate hiking cycle, borrowers with strong credit could find home equity loans below 4.5%. The dramatic shift upward caught many homeowners off guard, particularly those who delayed borrowing decisions. Rates peaked near 10% for prime borrowers in late 2023 before gradually declining to current levels.

Author: Hannah Whitlock;

Source: isomfence.com

Average Home Equity Loan Rates by Credit Score Range

| Credit Score Range | Typical Rate Range | Estimated Monthly Payment on $50,000 (15-year term) |

| Excellent (740+) | 6.75% – 8.00% | $447 – $478 |

| Good (670–739) | 8.25% – 9.50% | $485 – $522 |

| Fair (580–669) | 9.75% – 11.50% | $530 – $580 |

These estimates assume a loan-to-value ratio below 80% and standard underwriting. Your actual rate depends on multiple factors beyond credit score alone.

Regional variations exist but tend to be modest. Lenders in highly competitive markets like California or Texas sometimes offer rates 0.25% to 0.50% lower than those in less populated states, though online lenders have narrowed these gaps considerably.

Factors That Determine Your Home Equity Loan Rate

Credit score exerts the strongest influence on your rate. A 100-point difference—say, 680 versus 780—can shift your rate by a full percentage point or more. Lenders view higher scores as proof of reliable repayment behavior, which translates directly to lower risk and better pricing.

Your loan-to-value ratio (LTV) ranks second in importance. LTV compares your total mortgage debt (including the new home equity loan) to your home's current market value. If your home appraises at $400,000 and you owe $240,000 on your first mortgage, a $40,000 home equity loan brings your combined LTV to 70%. Most lenders offer their best rates to borrowers keeping combined LTV below 80%. Push above that threshold and expect rate premiums of 0.5% to 1.5%, plus potentially higher fees.

Author: Hannah Whitlock;

Source: isomfence.com

Debt-to-income ratio (DTI) measures your monthly debt obligations against gross monthly income. Lenders prefer DTI below 43%, though some accommodate higher ratios with compensating factors like exceptional credit or substantial cash reserves. High DTI doesn't always disqualify you, but it may add 0.25% to 0.75% to your rate.

The amount you're borrowing matters less than you might expect. A $25,000 loan and a $75,000 loan typically carry similar rates if your credit profile and LTV remain constant. However, very small loans under $10,000 sometimes face slightly higher rates because lenders' fixed processing costs represent a larger percentage of the loan amount.

Lender-specific policies create meaningful variation. Credit unions often beat banks by 0.25% to 0.50% because they operate as member-owned nonprofits with lower profit requirements. Online lenders fall somewhere in between, offering competitive rates but occasionally charging higher fees. Each institution sets its own risk appetite and pricing models, which is why shopping multiple lenders proves essential.

How to Compare Home Equity Loan Rates Across Lenders

The interest rate tells only part of the story. A lender advertising 7.25% might actually cost you more than a competitor quoting 7.50% once you account for origination fees, appraisal costs, and other charges. The APR incorporates these expenses into a single figure, making it the better comparison metric. A loan with a 7.25% interest rate but $3,000 in fees might carry a 7.65% APR, while a 7.50% rate with minimal fees could have a 7.55% APR.

Pay attention to these specific fee categories:

Origination or processing fees typically range from 0% to 3% of the loan amount. A 2% fee on a $50,000 loan adds $1,000 upfront. Some lenders waive these fees entirely to win business.

Appraisal costs run $400 to $600 in most markets. A few lenders cover this expense or use automated valuation models that eliminate the need for a physical inspection, though AVMs only work when recent comparable sales data exists.

Title search and recording fees add another $200 to $500. These costs vary by county and are harder to negotiate.

Rate lock periods protect you from increases between application and closing. A 30-day lock costs nothing with most lenders, but extending to 45 or 60 days may add 0.125% to your rate. If your closing timeline is uncertain, clarify lock terms upfront.

To get accurate quotes, request loan estimates from at least three lenders within a two-week window. Credit bureaus treat multiple mortgage-related inquiries within this period as a single event, minimizing the impact on your credit score. Provide identical information to each lender—same loan amount, same property value estimate, same income figures—so you're comparing apples to apples.

Red flags include lenders who refuse to provide written estimates, pressure you to decide immediately, or quote rates significantly below competitors without clear explanation. An outlier rate often comes with hidden fees or unrealistic qualification requirements that surface only after you've invested time in the application.

Borrowers who compare at least three lenders typically save 0.25% to 0.5% on their home equity loan rate, which can mean thousands in interest over the loan term. The lenders know when you're shopping around, and that competition works in your favor

— Jennifer Martinez

Fixed-Rate vs. Variable-Rate Home Equity Loans

Fixed-rate home equity loans dominate the market for good reason: payment predictability. Your rate and monthly payment never change, regardless of what happens to the Federal Reserve's policy rate, inflation, or broader economic conditions. This stability proves valuable when you're budgeting for long-term expenses or consolidating debt at a known cost.

The trade-off is that fixed rates typically start 0.5% to 1.0% higher than the initial rates on variable products. You're paying a premium for certainty. If rates decline substantially after you close, you're locked into the higher rate unless you refinance, which involves new fees and underwriting.

Variable-rate home equity loans adjust at specified intervals—commonly every quarter or year—based on an index like the prime rate plus a margin set by the lender. If prime is 6.50% and your margin is 1.50%, your current rate is 8.00%. When prime drops to 6.00%, your rate falls to 7.50%. The inverse also holds: rising prime rates push your payment higher.

Most variable products include rate caps that limit how much your rate can increase in a single adjustment period (periodic cap) and over the life of the loan (lifetime cap). A common structure might cap adjustments at 2% per year and 6% over the loan's life. These protections prevent payment shock but don't eliminate risk.

Choose a fixed rate when you're borrowing for a defined purpose with a clear repayment timeline and you value budget certainty above potential savings. Homeowners consolidating high-interest debt, funding a known renovation cost, or covering college tuition typically prefer fixed rates.

Variable rates make sense if you plan to repay the loan quickly—within three to five years—and can tolerate payment fluctuations. Some borrowers use variable products strategically, betting that rates will decline or planning to refinance before adjustment periods bring significant increases.

Tips to Secure the Lowest Home Equity Loan Rate

Improving your credit score before applying delivers measurable savings. If you're sitting at 695, delaying your application by three to six months while paying down credit card balances and disputing any report errors could push you above 720, potentially lowering your rate by 0.5% to 0.75%. On a $50,000 loan over 15 years, that's $30 to $45 less per month and $5,400 to $8,100 in total interest savings.

Target these specific credit improvements: reduce credit card balances below 30% of your limits (below 10% is even better), avoid opening new accounts in the six months before applying, and ensure all payments hit on time. One 30-day late payment can linger on your report for years and cost you dearly.

Shopping multiple lenders isn't optional if you want the best rate. Rate spreads between the highest and lowest offers for the same borrower commonly reach 1.0% to 1.5%. Three quotes represent the minimum; five is better. Include at least one credit union, one online lender, and one traditional bank in your search.

Author: Hannah Whitlock;

Source: isomfence.com

Negotiation works more often than borrowers expect. Once you have competing offers, return to your preferred lender and ask directly: "Lender X offered me 7.25% with a $500 origination fee. Can you match or beat that?" Loan officers have some pricing flexibility, particularly on fees. They'd rather trim their margin slightly than lose your business entirely.

Timing your application around Fed policy announcements rarely helps as much as people think. Markets price in expected rate changes weeks or months in advance, so waiting for an official Fed cut may mean you've already missed the best window. Focus instead on your personal readiness—strong credit, stable income, and clear borrowing purpose.

Lowering your LTV improves your rate and approval odds. If you're borderline at 82% combined LTV, borrowing $5,000 less or making a small principal payment on your first mortgage to drop below 80% can unlock better pricing. Some borrowers even use savings to pay down their primary mortgage temporarily, then replenish those funds with the home equity loan at a lower rate than they would have otherwise received.

Consider shorter loan terms if your budget allows. A 10-year term typically carries a rate 0.25% to 0.50% lower than a 15-year loan, and you'll pay dramatically less total interest. The monthly payment increases, but the overall cost savings can be substantial. Run the numbers both ways before deciding.

Frequently Asked Questions About Home Equity Loan Rates

Home equity loan rates represent just one component of a larger borrowing decision, but they're the component that most directly affects your long-term costs. A difference of even half a percentage point compounds into thousands of dollars over a 10- or 15-year term, making careful rate comparison and timing essential.

Start by strengthening your credit profile and clarifying exactly how much you need to borrow. Overestimating your needs costs you unnecessary interest; underestimating may force you into expensive secondary borrowing later. Request loan estimates from multiple lender types—credit unions, banks, and online platforms—within a concentrated timeframe to minimize credit inquiry impact while maximizing your negotiating position.

Pay close attention to the total cost of borrowing, not just the advertised rate. APR, fees, and loan terms combine to determine what you'll actually pay. A slightly higher rate with minimal fees often beats a rock-bottom rate buried in closing costs.

Fixed rates provide the predictability most borrowers need for major financial commitments. Variable rates introduce risk that only makes sense when you have a clear exit strategy or unusually high confidence in declining rate environments.

Your home represents your largest asset and most powerful financial tool. Borrowing against it demands the same careful analysis you'd apply to any major investment decision. The lenders offering the lowest rates and best terms won't find you—you need to find them through diligent comparison shopping and informed negotiation.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to home loans, mortgage rates, home equity loans, and the home buying process.

All information, including articles, guides, and explanations, is provided for general educational purposes only. Mortgage terms, interest rates, eligibility requirements, and lending conditions may vary depending on individual financial situations, lenders, and regional regulations.

This website does not provide financial, legal, or mortgage advice, and the information presented should not be considered a substitute for consultation with qualified financial professionals, lenders, or advisors.

The website and its authors are not responsible for any errors or omissions, or for any decisions made based on the information provided on this website.