Modern manufactured home on owned land with permanent residential appearance

Manufactured Home Loan Guide

Content

Content

Shopping for a manufactured home? You'll discover the financing process works differently than buying a stick-built house. Factory-built homes make up roughly 6% of America's housing inventory and cost 30-50% less per square foot than traditional construction, but getting approved for a loan involves extra steps most conventional buyers never encounter. The right financing choice—and there are more options than most people realize—determines whether you'll pay 6.5% or 10% interest, which translates to hundreds of dollars monthly on a typical loan.

Three factors control your financing path: whether you own the land underneath, how the home is classified legally (real property versus personal property), and what type of foundation supports the structure. Get these elements right and you'll access the same government-backed programs traditional homebuyers use. Miss one detail and you're stuck with limited options carrying significantly higher costs.

What Is a Manufactured Home Loan?

Financing exists specifically for homes constructed completely inside a factory, then moved to a permanent or semi-permanent location. Federal law requires these structures to meet the Manufactured Home Construction and Safety Standards—commonly called the HUD Code—which took effect June 15, 1976. You'll spot compliant homes by the red certification label attached to the exterior, usually near the back corner. Lenders won't approve applications without verifying this label exists and remains legible.

Here's how different factory-built housing types break down:

Manufactured homes roll off production lines after June 15, 1976, arrive in one or more sections loaded on truck chassis, and follow HUD Code specifications rather than local building requirements. You can set them on land you purchase or rent a space in a dedicated community.

Mobile homes came before the 1976 regulations kicked in. Banks rarely finance these older units because they lack modern safety features and energy efficiency standards. Even sellers accepting owner financing charge premium interest rates on pre-HUD-Code units.

Modular homes also ship from factories but comply with the same International Residential Code that governs stick-built houses. Once crews set the modules on a permanent foundation and complete hookups, these structures function identically to site-built homes—and qualify for standard mortgage products without jumping through extra hoops.

The financing distinction matters because lenders categorize manufactured homes in two ways. Treat the structure as real property—meaning permanently attached to land parcels—and you'll access traditional mortgage products with competitive rates. Classify it as personal property (similar to financing a boat or RV) and you'll face chattel loans with steeper costs and tighter terms.

This landscape shifted when Fannie Mae rolled out MH Advantage during 2019, followed by Freddie Mac's CHOICEHome program in 2021. Both initiatives brought conventional financing to manufactured homes meeting upgraded construction specs, which narrowed—though didn't eliminate—the gap between manufactured and traditional home loan costs.

Author: Hannah Whitlock;

Source: isomfence.com

How Manufactured Home Financing Works

The approval process mirrors traditional home buying with additional verification checkpoints. Your lender confirms HUD certification, examines foundation type and installation quality, then determines whether state records list the structure as real or personal property.

Once pre-approved, you'll hunt for a home meeting your lender's criteria. Sellers or manufacturers supply paperwork proving HUD compliance—the original red label location, installation records, and manufacturer specifications. Your lender orders an appraisal next, though finding qualified manufactured home appraisers takes longer than traditional appraisals. Expect delays of one to three weeks in rural markets where fewer appraisers work.

Appraisers check the home's current condition, confirm permanent foundation installation when required, and verify proper titling. Title research gets complicated with manufactured homes because states originally issued vehicle titles through DMV offices rather than recording real property deeds at county offices. Older homes might carry outstanding liens, unpaid community fees, or ownership clouds that surface during title work.

Closing procedures resemble traditional mortgages for mortgage-classified loans, including title insurance and deed transfers. Chattel loans skip some steps since no real estate changes hands, which speeds up closing but also eliminates title insurance protection.

Chattel Loans vs. Mortgage Loans

This classification determines everything about your financing costs and monthly budget. Chattel loans treat manufactured homes as personal property—think car loans applied to housing. You can secure chattel financing whether you own land, lease a community space, or plan installing the home on a family member's property.

Current chattel rates run between 7.5% and 10.5% throughout 2026—substantially higher than mortgage products—because lenders face elevated risk. Homes can be relocated, they depreciate more aggressively than site-built properties in most markets, and repossession requires less legal process than foreclosure. You're also looking at maximum terms around 15 to 20 years rather than the standard 30-year mortgage, which pushes monthly payments higher even before accounting for interest rate differences.

Mortgage loans reclassify homes as real property after permanent attachment to land you own. The structure needs an approved foundation system, and you'll complete your state's title retirement process that removes the DMV vehicle title and records the home as part of the land parcel. This conversion unlocks conventional mortgage products, government-backed programs offering superior terms, and interest rates currently ranging from 6.0% to 8.0% in early 2026.

Author: Hannah Whitlock;

Source: isomfence.com

Land Ownership Requirements

Your loan program determines whether you need to own the land beneath your home. FHA Title I chattel loans skip land ownership requirements entirely—lease a lot in a manufactured home park and you're eligible. However, borrowing caps out at $69,678 for single-section homes or $130,357 for multi-section units under 2026 limits.

FHA Title II, VA, USDA, plus all Fannie Mae and Freddie Mac programs mandate land ownership. You'll either finance land and home together in one transaction, or already own the property outright before applying. Some lenders accept simultaneous land-home purchases while others impose waiting periods of six to twelve months between land acquisition and home financing.

Combined land-home financing triggers additional underwriting. Lenders evaluate the land's market value, road access, zoning compliance, and utility availability. Rural parcels often need well water testing and septic system inspections before approval. Note that mortgage programs won't finance homes in leased-lot communities regardless of foundation quality—those scenarios always require chattel loans.

Loan Options for Manufactured Homes

Multiple financing programs serve manufactured home buyers, each carrying distinct eligibility rules and benefits.

FHA Title I loans deliver chattel financing without land ownership requirements. Single-section homes qualify for up to $69,678, multi-section units reach $130,357, and you can borrow $23,226 for developed lot purchases. These loans accept credit scores starting around 580 but charge elevated interest rates and limit repayment periods compared to mortgage products. Your home must serve as your primary residence and display HUD certification, though foundation specifications are less demanding than mortgage programs require.

FHA Title II loans operate as standard mortgages when you own the land underneath. Homes need real property classification, installation on FHA-approved permanent foundations, and construction dates after June 15, 1976. You'll put down 3.5% minimum with a 580 or higher credit score. County-specific loan limits mirror standard FHA caps, starting at $498,257 and exceeding $1 million in expensive markets during 2026. Properties must satisfy FHA's Permanent Foundation Guide for Manufactured Housing, which details foundation engineering, anchoring specifications, and frost protection in cold climates.

VA loans deliver zero-down financing for qualifying veterans and active service members. Homes must carry real property status, permanent attachment to land you own, and post-June 15, 1976 construction. Most borrowers face no maximum loan limits under 2026 VA guidelines, though individual lenders may cap loans based on their portfolio risk. Foundation specs match FHA standards. VA loans typically deliver the lowest rates among government programs—often running one-quarter to one-half percent below comparable FHA products.

USDA loans provide full financing for qualifying rural properties. Both land and home must sit in USDA-eligible zones (typically communities under 35,000 population), while your household income can't exceed 115% of area median income. Homes can be new or existing inventory, require real property status, and need permanent foundations. USDA rates compete favorably with other programs but add a 1% upfront guarantee fee plus ongoing annual fees at 0.35% of your remaining balance.

Fannie Mae MH Advantage opened conventional financing to manufactured homes exceeding basic construction standards. Qualifying homes must be multi-section units on permanent foundations with real property classification, meeting architectural requirements including 12-foot minimum width, residential-style roof slopes of 3:12 or steeper, and no visible wheels, axles, or towing hitches. First-time buyers put down 3% while repeat buyers need 5%. Credit scores typically start at 620, and underwriters approve debt-to-income ratios reaching 50% with strong compensating factors.

Freddie Mac CHOICEHome delivers similar advantages to MH Advantage with slightly different construction specs. Single-section homes need at least 600 square feet while multi-section units must hit enhanced design benchmarks. Down payments begin at 3%, and loan caps follow conventional conforming limits—$806,500 across most counties in 2026.

Conventional lender programs vary dramatically between institutions. Some credit unions and community banks maintain portfolio loans for manufactured homes missing Fannie Mae or Freddie Mac qualifications. These loans might accept older inventory from the 1990s or newer, homes on leased lots, or properties missing enhanced construction features. Rates and terms scatter across a wide range, making lender shopping essential.

Author: Hannah Whitlock;

Source: isomfence.com

Manufactured Home Loan Requirements

Each program enforces specific borrower and property standards.

Credit score minimums span from 500 to 700 depending on which program you choose. FHA Title I accepts scores starting at 500 with 10% down, though most lenders set internal floors around 580. FHA Title II wants 580 for the 3.5% down payment option or 500 if you'll put down 10%. VA loans lack official score minimums, but most lenders won't approve applications below 580 to 620. USDA typically wants 640 for automated underwriting approvals. Conventional products (MH Advantage and CHOICEHome) generally require 620 as a starting point, with better pricing appearing above 700.

Down payment expectations shift by program. VA and USDA offer zero-down options for eligible applicants. FHA Title II asks 3.5% down when credit scores hit 580 or higher, or 10% down for scores between 500 and 579. Conventional programs require 3% to 5% down for owner-occupied purchases. Chattel loans typically demand 5% to 20% down, with higher amounts required for older homes or applicants carrying lower credit scores.

Debt-to-income ratios compare your total monthly debt payments against gross monthly income. FHA approves ratios reaching 43% without compensating factors, or stretches to 50% for borrowers showing strong credit and cash reserves. VA demonstrates flexibility, regularly approving ratios above 50% when borrowers maintain good credit and sufficient residual income. USDA caps housing expense ratios at 41% and total debt ratios at 46%. Conventional programs typically max between 45% and 50% based on your credit score, down payment size, and reserve funds.

Property standards extend well beyond basic HUD certification. FHA Title II requires minimum 400 square feet, post-June 15, 1976 construction, and real property classification. Homes need permanent foundations meeting FHA engineering standards—proper anchoring, support piers spaced per manufacturer specifications, and enclosed crawl spaces.

VA imposes similar standards plus verification that homes satisfy local building codes. Some jurisdictions layer on additional inspections or permits beyond HUD certification requirements.

MH Advantage and CHOICEHome add enhanced construction standards covering minimum roof pitch, residential-style exteriors, covered entry areas, and attached garages or carports. These programs reject homes showing visible wheels, axles, or towing tongue assemblies.

Author: Hannah Whitlock;

Source: isomfence.com

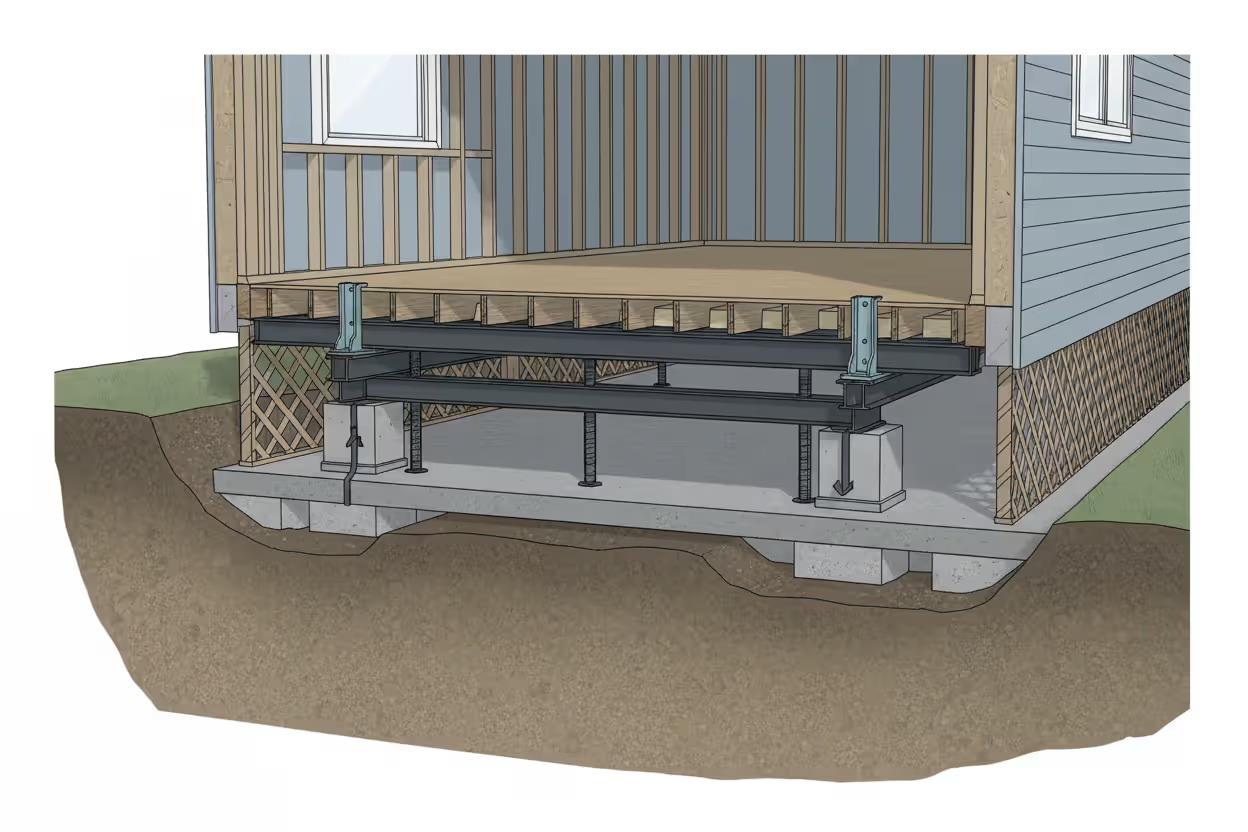

Foundation requirements represent where most loan applications fail. Permanent foundations must be engineered systems supporting the home's total weight, resisting wind and seismic forces per local building codes, and following manufacturer installation instructions precisely. Acceptable systems include reinforced concrete slabs, crawl spaces with masonry or poured concrete perimeter walls, and full basement foundations.

Pier and beam systems must follow specific spacing requirements dictated by home dimensions and weight, use approved pier materials like concrete, masonry, or engineered wood, and incorporate proper anchoring straps connecting the frame to ground anchors. Foundations need adequate drainage, moisture barriers meeting local codes, and frost protection in regions where ground freezes.

Homes sitting on leased land in manufactured home communities rarely qualify for mortgage programs regardless of foundation quality, limiting buyers to chattel loans.

Interest Rates and Costs for Manufactured Housing Loans

Too many borrowers assume traditional mortgages aren't available for manufactured homes, so they accept chattel loan terms without exploring alternatives.When you own the land and your home meets foundation requirements, switching from chattel to FHA or conventional mortgage financing typically saves $200 to $400 every month

— Jennifer Martinez

Manufactured home loan rates currently run one-half to two and one-half percentage points above comparable site-built home mortgages. Throughout early 2026, borrowers with solid credit securing mortgage loans for manufactured homes on owned land see rates between 6.0% and 8.0%, while traditional home rates range from 5.5% to 7.0%.

Why the rate gap? Manufactured homes historically lost value faster than stick-built properties, though well-maintained units on permanent foundations in strong markets now appreciate at comparable rates. The secondary market for manufactured home loans remains smaller, meaning lenders can't easily sell these mortgages to investors, which increases their capital costs. Historical default rates ran higher for manufactured home loans, though recent performance data shows loans meeting Fannie Mae and Freddie Mac standards default at similar rates to traditional mortgages.

Chattel loans carry substantially higher rates—currently 7.5% to 10.5%—reflecting the personal property classification and elevated risk profile. These loans also charge steeper origination fees, typically 3% to 5% of your loan amount compared to 1% to 2% for mortgage loans.

Closing costs for manufactured home mortgages mirror traditional home purchases: origination fees, appraisal charges ($400 to $700), title insurance premiums, recording fees, and prepaid items like property taxes and insurance. Budget for total closing costs between 2% and 5% of your loan amount. Chattel loans carry lower closing costs by skipping title insurance, but higher origination fees usually cancel out these savings.

Insurance requirements include homeowners coverage protecting the structure and providing liability protection. Properties in flood zones need separate flood insurance policies. Lenders require coverage amounts matching either your loan balance or the home's replacement cost, whichever is higher. Manufactured home insurance can run 15% to 30% more than site-built home coverage in some markets, though homes meeting enhanced construction standards and sitting on permanent foundations often qualify for standard homeowners policies with competitive pricing.

| Loan Program | Down Payment Required | Minimum Credit Score | Must Own Land? | Current Rate Range (2026) | Maximum Loan |

| FHA Title I (Chattel) | 5% to 10% | 580+ (or 500+ with larger down payment) | No | 7.5% to 10.5% | $69,678 single / $130,357 multi-section |

| FHA Title II (Mortgage) | 3.5% to 10% based on credit | 580+ (or 500+ with 10% down) | Yes | 6.25% to 7.75% | $498,257 to $1,149,825 (varies by county) |

| VA Loan | Zero down | No set minimum (lenders typically want 580-620) | Yes | 6.0% to 7.5% | No cap for most borrowers |

| USDA Loan | Zero down | 640+ preferred for automated approval | Yes | 6.25% to 7.5% | Income-based limits apply |

| Conventional (MH Advantage / CHOICEHome) | 3% to 5% | 620+ | Yes | 6.5% to 8.0% | $806,500 in most counties |

Common Mistakes When Financing a Manufactured Home

Accepting chattel financing when you qualify for a mortgage wastes thousands of dollars over your loan's life. Consider a $150,000 chattel loan at 9% over 20 years—you'll pay $1,350 monthly with $174,000 in total interest. Finance that same amount through an FHA mortgage at 6.75% over 30 years and you'll pay $973 monthly with $200,280 total interest. Yes, you'll pay more interest over the full 30 years, but the lower monthly payment frees up $377 for other expenses or savings.

Skipping foundation verification before purchasing kills deals after you've invested in inspections and appraisals. Confirm foundation type before writing an offer. Homes sitting on blocks or inadequate pier systems need foundation upgrades costing $8,000 to $20,000. Many sellers won't invest in foundation improvements, leaving you without financing options.

Not researching lender restrictions eliminates good financing options unnecessarily. Some lenders maintain blanket policies refusing all manufactured home loans regardless of condition or foundation quality. Others restrict financing to homes built after 1990 or 2000, even though FHA and VA accept any post-1976 HUD-certified home. Call lenders directly before applying to confirm they'll finance manufactured homes matching your property's specifications.

Missing HUD certification verification derails closings at the worst possible time. The red HUD certification label must be physically present and readable. When labels disappear during renovations or fade from weather exposure, you'll need to obtain certification verification from either the manufacturer or the Institute for Building Technology and Safety (IBTS)—a process taking weeks and costing $300 to $500.

Bypassing title searches creates legal nightmares down the road. Manufactured homes may carry liens from previous owners, unpaid community fees, or title problems from improper transfers. Unlike real property transactions where title insurance catches these issues, chattel loans may not include title searches, leaving you exposed to claims against the home.

Ignoring manufactured home community restrictions hurts resale options later. Some communities restrict which financing types buyers can use, prohibit certain lenders from operating in the park, or charge substantial transfer fees that shrink your buyer pool. Review all community rules before purchasing, paying special attention to age restrictions, pet policies, and rental prohibitions affecting future marketability.

Author: Hannah Whitlock;

Source: isomfence.com

Frequently Asked Questions About Manufactured Home Loans

Successfully financing a manufactured home depends on understanding chattel versus mortgage loan differences, matching your situation to the right program, and ensuring your property satisfies foundation and classification requirements. Buyers owning land who can install homes on permanent foundations gain access to dramatically better rates and terms through FHA, VA, USDA, or conventional mortgage programs. Buyers purchasing homes in leased-lot communities face chattel loan limitations but can still reach homeownership with careful planning and realistic budgeting.

The manufactured housing finance landscape improved dramatically when Fannie Mae and Freddie Mac launched their enhanced programs, shrinking—though not eliminating—the cost gap between manufactured and site-built home financing. Success still requires partnering with experienced lenders who understand manufactured home requirements, verifying HUD certification and foundation compliance before writing offers, and comparing multiple loan options to secure the best terms for your specific property and financial circumstances.

Investing time to understand these financing fundamentals, sidestepping common mistakes, and selecting the optimal loan program can save tens of thousands of dollars while making manufactured home ownership an affordable and sustainable path toward building equity and long-term housing stability.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to home loans, mortgage rates, home equity loans, and the home buying process.

All information, including articles, guides, and explanations, is provided for general educational purposes only. Mortgage terms, interest rates, eligibility requirements, and lending conditions may vary depending on individual financial situations, lenders, and regional regulations.

This website does not provide financial, legal, or mortgage advice, and the information presented should not be considered a substitute for consultation with qualified financial professionals, lenders, or advisors.

The website and its authors are not responsible for any errors or omissions, or for any decisions made based on the information provided on this website.